Ever since man learned to build, he has been striving to reach higher. The instinct to construct – to leave something behind that outlasts us – has defined every era. From the Tower of Babel and the Pyramids of Giza, humanity’s first brush with vertical ambition, to the palaces of Udaipur, where marble met imagination, and the stone castles of Europe that turned defence into legacy – every structure has reflected the aspirations of its age.

Centuries later, that instinct remains unchanged. Only the skylines have evolved. The Burj Khalifa in Dubai, the Shanghai Tower, even Mumbai’s Bandra-Worli Sea Link – all stand as modern symbols of progress and persistence. We’ve moved from stacking stones to forging steel, but the impulse remains the same: to build higher, to build better, to build meaning.

Nowhere is this more visible today than in India’s cities. Make no mistake, real estate investment is no longer about homes alone. Anyone who’s walked through BKC in Mumbai, Whitefield in Bengaluru, or Cyber City in Gurgaon can see it – the wheel of commercial real estate is spinning fast. Office towers rise where empty plots once stood. Glass façades mirror the country’s growth. Everyone wants a piece of this momentum, quite literally.

The problem? It’s expensive. That’s always been real estate’s paradox – alluring and tangible, yet accessible only to those with deep pockets. Not anymore. Enter Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs) – innovative financial instruments that marry the entrepreneurial drive of builders with the capital of investors. A structure that finally makes it possible for ordinary investors to own a fraction of India’s growth story, one building, or one bridge, at a time.

What are REITs / InvITs

REITs (Real Estate Investment Trusts) and InvITs (Infrastructure Investment Trusts) are investment vehicles that allow investors to invest in real estate and infrastructure assets respectively, without owning the physical property. Simply put, REITs invest in completed and under-construction real estate projects whereas InvITs invest in infrastructure projects.

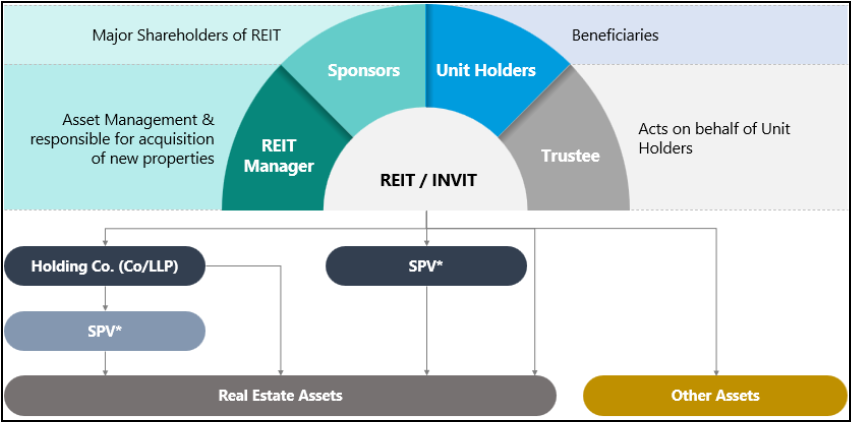

Exhibit 1- Structure

*SPV- Special Purpose Vehicle

In many ways, REITs and InvITs are like mutual funds for real assets. Instead of pooling money to buy stocks or bonds, they pool investor capital to own income-generating real estate or infrastructure projects. Each unitholder owns a fractional share in the trust’s portfolio — much like mutual fund investors own a share of the underlying securities. The difference simply lies in the asset class: where mutual funds give exposure to financial markets, REITs and InvITs open the door to India’s offices, malls, roads, and power lines.

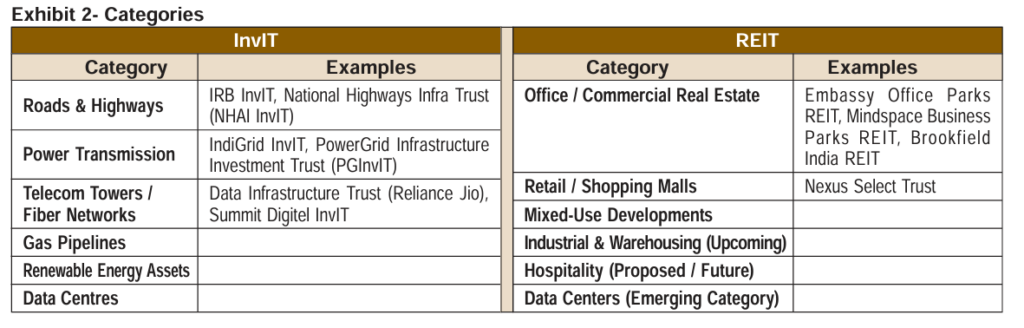

Categories and examples

Within the Infrastructure segment, InvITs focus on categories like roads and highways, power transmission etc. Similarly, REITs look at commercial real estate. Current regulations mandate that each instrument (InvIT or REIT) must focus on a single category and doesn’t have an amalgamation of different categories.

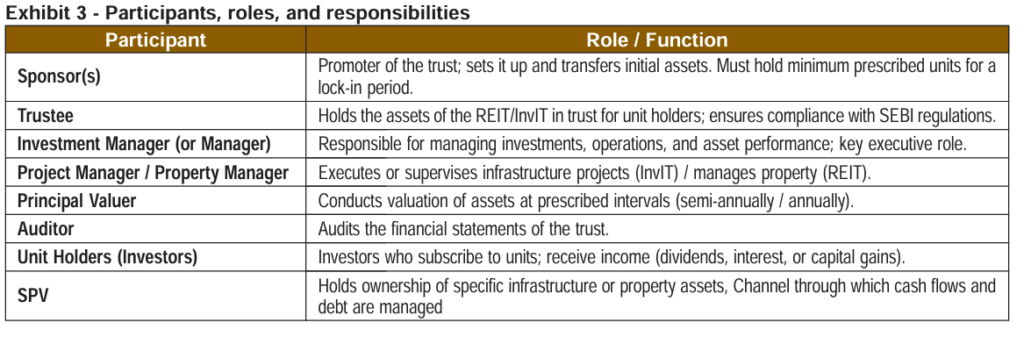

For each of these instruments, the participants and their role & functions are similar in nature.

An SPV is a subsidiary company or LLP formed by the Sponsor specifically to own and operate a particular project or asset. In an InvIT or REIT structure, the trust does not directly own the physical assets — it owns shares or units in the SPVs that hold those assets.

Given that both REITs and InvITs have a lot of commonalities, the regulations for many aspects are common to both of them. For instance, within their own focused segment:

Investment

- Minimum of 80 percent of the investment has to be done in completed income/revenue generating properties / Infrastructure projects.

- A maximum of 20 percent of the investment is permitted in under-construction projects, debt or government or money market instruments is permitted.

Distribution

- A minimum of 90 percent of the Net Distributable Cash Flows (NDCF) have to be distributed to unit holders. This must be distributed once every six months. However, in practice, REITs and InvITs distribute them every quarter, within 15 days from the date declared by the manager.

- These components typically consist of dividends, interest on loans given to SPVs, etc., which are disclosed to unitholders.

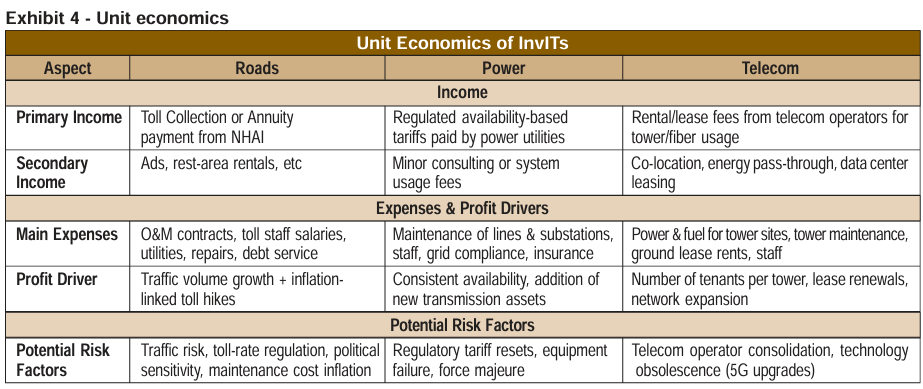

Now that we have a broad overview of each of these instruments, it’s important to understand how these instruments make money.

The scale of a global idea

Real estate trusts aren’t new. The first REITs appeared in the US in the 1960s, born out of a simple idea – to let small investors participate in large, income-generating properties without having to buy them outright. Since then, the model has gone global.

Today, more than 40 countries have REIT regimes, collectively managing over $3.5 trillion in assets. The United States remains the largest market, accounting for nearly two-thirds of global REIT capitalization, with giants like Prologis, Equinix, and Simon Property Group defining the space. Mature markets like Singapore and Australia have turned REITs into institutional favourites, where pension and sovereign funds treat them as core allocations rather than niche alternatives.

InvITs – the infrastructure counterpart – followed a similar path. The world’s first InvIT-like structures emerged in developed markets under names like Infrastructure Trusts or Public–Private Partnership Funds. Together, these vehicles now finance airports, highways, renewable grids, and data centres across continents.

Vocal For Local

India’s REIT and InvIT journey began much later – the enabling regulations came only in 2014, with the first listing (Embassy Office Parks REIT) in 2019. Yet, the pace of growth since has been brisk.

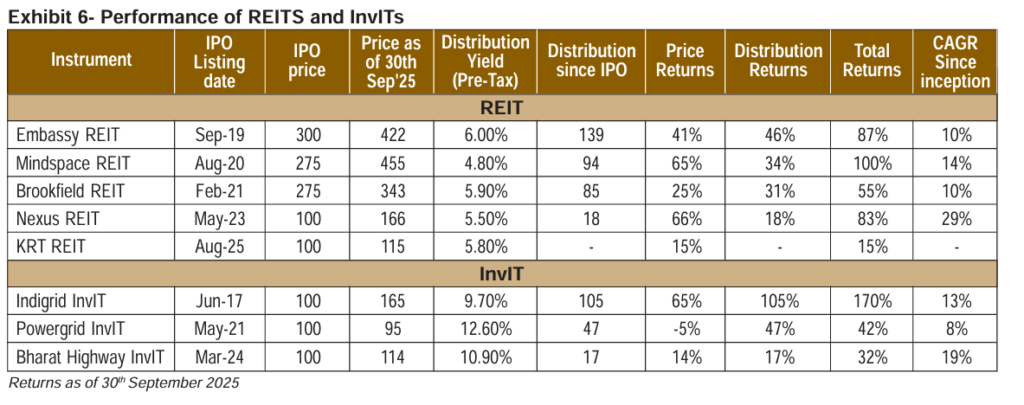

As of late 2025, India’s REIT market comprises four long-standing listed REITs – Embassy Office Parks, Brookfield India, Mindspace Business Parks, and Nexus – with a fifth entrant, Knowledge Realty Trust (KRT), recently listed. This brings the total to five publicly listed REITs. Together, these trusts own or manage over 115–130 million square feet. of Grade-A commercial real estate across major Indian cities. The approximate assets under management at a gross level stand at around Rs. 1.63 lakh crores whilst the market capitalisation stands at around Rs. 1 lakh crore (as of Sept 2025).

On the infrastructure side, eight InvITs are listed, spanning roads, power transmission, and telecom. Overall, India has around 26 registered InvITs (public and private) and between them, they manage assets worth over Rs.7 lakh crore, representing more than 35,000 lane-kilometres of roads and 30,000 circuit-kilometres of power transmission lines.

For a country where real estate and infrastructure have long been synonymous with illiquidity, opacity, and high entry barriers, this is a quiet revolution. REITs and InvITs have turned hard assets into tradeable, regulated, and income-yielding securities – a bridge between India’s skyline and its stock market.

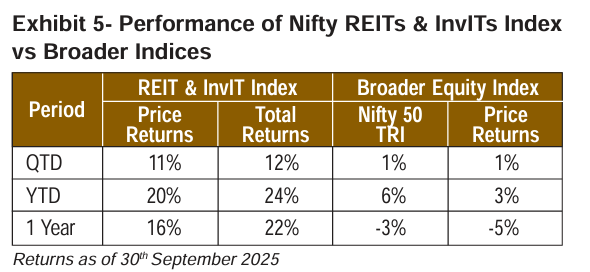

Performance

For all the talk around accessibility and yield, REITs and InvITs are ultimately judged by how they perform against traditional assets. In India, their progress is now trackable through the Nifty REITs & InvITs Index (Factsheet_REITs_InvITs.pdf), which offers a snapshot of how these income-generating trusts stack up against the broader equity market. The index is diversified across realty 73.7 percent, Power 18.7 percent, Services 6.49 percent, and Construction 1.09 percent with a total of 9 constituents.

Typically, Managers declare per-unit distributions with a breakup across interest, dividend, and loan repayment – these form the components of the pre-tax distribution yield.

To calculate the post tax calculation, it is necessary to look at each component separately.

- Dividend- If the SPV has opted for a lower corporate tax u/s 115BAA, then the dividend is taxable at the investors income slab rate. Whereas, if the SPV has not opted for a lower corporate tax, then the dividend is exempt in the hands of the investor.

- Interest as a component is taxable as per the investors income slab rate.

Therefore, the net distribution yield can vary depending on the breakup of the distribution.

Sale of Units (current tax regime)- Capital gains will be taxed at-

- Sold Off-market (unlisted or without paying STT)- As per tax slab if held for <24 months and 12.5% for more than 24 months

- Sold on stock exchange (listed units with STT paid)- 20% if held for <12 months and 12.5% for more than 12 months

Regulatory developments

It’s taken time for India’s REITs and InvITs to find their footing. The concept was simple enough – fractional ownership in large, income-generating assets, but the regulations took a while to catch up.

For years, both were parked under SEBI’s “hybrid” category – an uneasy middle ground between equity and debt. Mutual funds could invest in them, but with caveats. It was a nod to prudence, but it also kept the flow of capital modest. Fund houses that wanted to participate had to explicitly amend their scheme documents to make room for these assets.

That’s now changing. In September 2025,

- SEBI reclassified REITs as equity instruments, aligning India with global practice. InvITs, however, will remain hybrids for now.

- The shift is more than a technicality – it allows equity and hybrid mutual funds to count REIT exposure as part of their equity allocation, opening a much larger pool of institutional capital. In the long run, it could mean deeper liquidity, better price discovery, and more listings — the three things every young market needs.

For now, Indian REITs are restricted to commercial real estate – offices, business parks, and malls. Globally, REITs have long covered residential and even healthcare properties. If Indian regulations evolve in that direction, the next wave of REITs might not just own the offices we work in, but the homes we live in.

Investor options and realistic expectations

For a long time, the only doorway into commercial real estate was reserved for HNIs and ultra-HNIs. They entered through Category II AIFs – private investment pools that bought into the same kind of offices and malls now found in listed REITs. The intent was similar, but the structure and accessibility couldn’t have been more different.

A Category II Commercial Real Estate AIF typically:

- Focuses on pre-leased properties with long-term tenants.

- Has a finite tenure, after which the asset is sold and proceeds distributed.

- Invests in a concentrated pool of assets – often just a few high-value buildings.

- Can use leverage to enhance returns.

- Does not distribute payouts regularly; cash flows are usually reinvested until exit.

These features make AIFs suited to investors seeking higher but riskier returns- those comfortable with illiquidity and project-specific exposure.

REITs and InvITs, by contrast, are listed, yield-oriented, and standardised- closer to a commoditised version of real estate investing. Investors should approach them with realistic expectations. These are not the “my-uncle-bought-a-plot-and-became-a-crorepathi” stories that dominate Indian dinner tables. Their value lies in steady income and regulated transparency, not windfall appreciation.

That doesn’t mean they’re risk-free. Government regulation, interest-rate cycles, market volatility, sectoral demand, and valuation assumptions all influence their performance. While REIT and InvIT units trade daily on exchanges, their Net Asset Value (NAV) is calculated only every six months by an independent valuer certified and registered with SEBI. This NAV acts as a benchmark to gauge whether the units trade at a premium or discount, typically expressed through the Price-to-NAV ratio.

In essence, the market price reflects investor sentiment, not the underlying appraised value – which means price moves are driven by demand and liquidity, not a daily NAV like in mutual funds. For investors, this translates into one simple truth: these instruments offer liquidity, but not immunity from market mood.

For most investors, REITs and InvITs sit somewhere between equity and fixed income – they offer the stability of recurring cash flows with a dash of market-linked upside. In a diversified portfolio, a 5 to 10 percent allocation can serve as an effective income anchor, especially for those seeking regular distributions without locking money into traditional debt products.

For retirees or investors aiming to build a steady income stream, these instruments can complement fixed deposits or debt funds – with one key difference: the underlying assets are real and often inflation-linked through rent escalations or tariff adjustments.

Back to the pavilion

If you’ve made it this far, thank you – this has been a long read, and we’ve tried to make it worth your time. Some topics resist quick summaries. REITs and InvITs are among them. They sit at the intersection of finance, infrastructure, and aspiration – and understanding them means going a few levels deeper than the usual headlines. Our goal wasn’t to explain just what they are, but why they matter – how they’re changing the way India owns, builds, and participates in its own growth story.

If we had to draw a cricketing parallel, REITs are like the solid middle-order batsman – dependable, steady, quietly accumulating runs over time. InvITs, on the other hand, play a bit more like the all-rounder – capable of big hits through leverage and risk, but needing the right conditions to shine. Neither is flashy, neither is meant for a quick sprint. But both, in their own way, help the team win over the long haul.

If you think about it, the timing feels poetic. As India’s team heads to Australia for yet another Test series, we’re reminded that patience, discipline, and adaptability win matches – not just talent. The middle order has its dependable run-accumulators; the all-rounders, like Jadeja and Hardik, bring balance and spark – much like REITs and InvITs in an investment portfolio. They may not dominate every session, but they hold the innings together and create opportunities when it matters most.

And just as we’ll all be hoping the boys return from Australia with a series win, investors can hope these instruments – steady, measured, and quietly compounding – continue to perform well for those betting on India’s broader growth story. Because in finance, as in cricket, the long game is where the real stories are made.