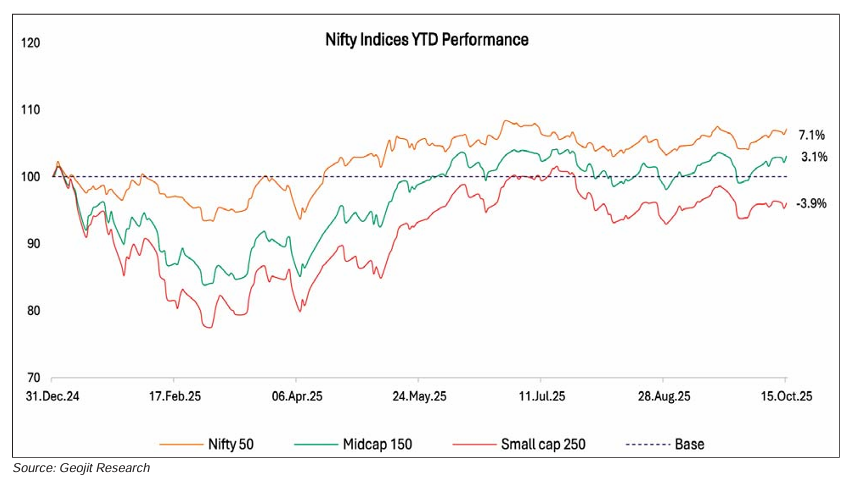

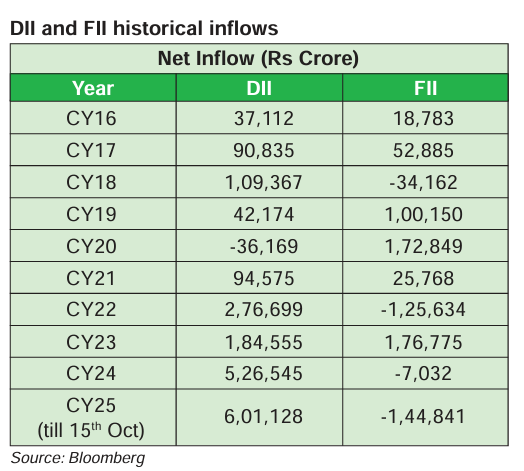

Year till date, as on 15th October, the Indian equity market has delivered a modest 7.1 percent return on the Nifty50 index. Concurrently, the broader market has remained weak, with subdued performance across mid- and small-cap stocks. The last two years have been challenging for domestic investors, who have continued their steady investments despite muted returns. DII’s annual investment reached Rs 6 lakh crore, which is 6 times the annual average before 2023.

Similarly, retail investors have shown remarkable patience and conviction over the past two years despite challenging market conditions. However, their direct participation in the secondary market has softened recently, driven by the continued underperformance of Indian equities compared to global peers and alternative assets such as gold. To revive sentiment and sustain momentum, a return of foreign investors is essential. Over the past 12 months, FIIs have sold more than Rs.2.5 lakh crore, redirecting funds toward markets with lower valuations, opportunities in AI and semiconductors, and trade-linked advantages. However, going ahead, plausibility is arising that FII outflows could ease and turn positive, as the premium valuation of India has reduced to below the long-term average and earnings are to rebound from Q3 onwards.

After a phase of stagnation, India economy and stock market now stand at an inflection point. Over the past four quarters, corporate earnings growth has remained muted despite stable economic expansion of 6 to 7 percent. This is because of the reduction in global inflation and growth after the high growth during 2022-24, impacting realization and profitability. Tax cuts, GST reforms, and a decline in CPI inflation are expected to boost domestic demand, triggering earnings growth from Q3FY26 onwards. EPS growth sustained in 2026 augurs well for the market.

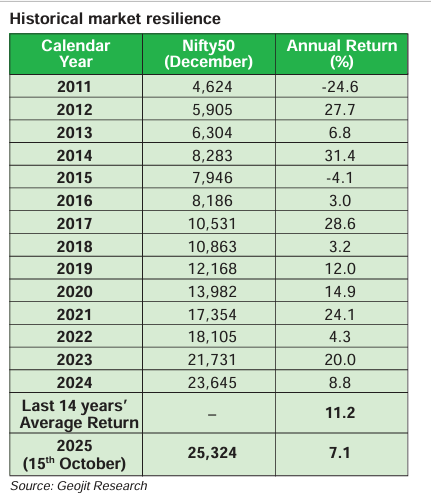

Resilience of India in a volatile 2024–25 market

India has provided an average return of 11.2 percent in the last 14 years. The market has generally posted positive yearly returns, with exceptions primarily arising from global disruptions such as the US financial crisis in 2009, the European sovereign debt crisis of 2010–11, the sluggish US economic recovery in 2013 due to high debt, the Fed’s tightening policy in 2015, the Chinese market crash in 2015–16, and the Greek debt crisis in 2015.

Following a strong performance in 2023, driven by robust real GDP growth of 8.2 percent in FY24, declining crude prices, and a revival in domestic inflows, the Indian market’s momentum softened in 2024 and early 2025, ahead of the national and state elections. This weakness intensified as FII selling picked up, prompted by India’s premium valuations. “Sell India, buy China” led as the strategy of 2024-25. Loss of new opportunities like semiconductors and AI, led to a deficit in India’s story escalating FIIs to shift to tech-based nations like the US, China and Taiwan.

On the positive side, even amid challenging conditions, India delivered respectable nominal returns of 8.8 percent in 2024 and 7.1 percent in 2025 (as of 15th October). The last 12 – 15 months have been particularly difficult for the domestic market, facing unexpected setbacks ranging from tariff changes to geopolitical tensions. However, going ahead risks like low earnings growth and tariff problems are expected to be reduced, setting the stage for improved market performance by year-end.

Large caps are the savers

During the challenging period of 2025, large caps provided modest returns while mid- and small caps remained highly selective, making investing more difficult. Identifying attractive opportunities has been particularly challenging in 2024–25. We expect large caps to continue to have the upper hand in the short to medium-term as risk appetite continues to be low and their businesses are much more stable. Mid-caps, however, are likely to gain momentum as earnings growth resumes and FII selling moderates.

Certain sectors performed well, such as metals due to supply and tariff constraints elevating realisation; auto rallied on expectations of GST benefits; and financials did well due to reduction in unsecured loan stress and accommodative monetary policy. Conversely, weaker sectors like IT and Pharma are likely to remain subdued in the near term due to external risks, though they present potential long-term opportunities. Similarly, reality and consumption spaces are expected to be better in 2026 due to signs of revival in ground reality.

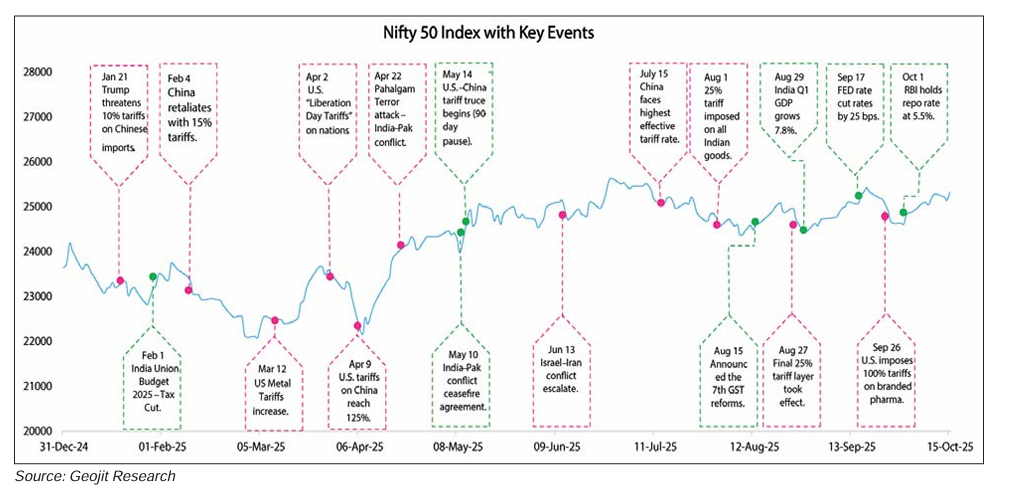

The unexpected twist of 2025

Along with the continuation of FII selling, 2025 brought many unexpected events and risks. The most significant challenges included abrupt shifts in US policy under Trump, moving from a pro-India to an anti-India stance, resulting in India being subjected to some of the highest tariffs. Heightened geopolitical tensions—from Russia-Ukraine and Israel-Hamas conflicts to Indo-Pak tensions—further added volatility to both global and Indian markets. Global investors reacted negatively to protectionist trade policies, leading equities to underperform, while safe-haven assets like gold surged, rising nearly 60 percent in India over the past year.

Lately, the Trump narrative has moderated when the US market took a dip; however, the policy continues to hang as a burden. Progress in Israel-Hamas peace and a change in the Fed’s tone to cut rates and liberalize the quantitative tightening policy have provided a push to world equity lately. Additionally, Indo-US trade talks are reportedly advancing, with a mini-deal expected by the end of November. If these developments materialize as anticipated, the year could close on a relatively strong note.

Domestic investors focused on long term growth to gain real benefits

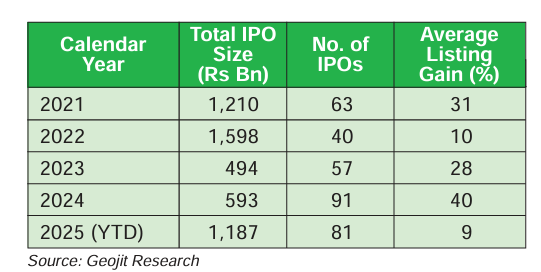

Domestic investors have a long-term view of the India economy. In the last 2 years, DIIs have invested Rs 11.3 lakh crore, which is 40 percent more than the total amount invested during the 8 years from CY16 to CY23. This conviction is likely to be reinforced in CY26, supported by steady monthly SIP inflows; however, overall market performance could be influenced if lump-sum investments moderate due to external challenges. The performance of the secondary market is also impacted by the high number of IPOs. In CY25, the primary market attracted Rs 1.2 lakh crore funds, which is more than the amount raised in CY23 and CY24, while listing gains have been modest due to the fall in the quality of IPOs.

Primary market trends and IPO performance

In the near-term, higher household spending during the festive season, coupled with the continued underperformance of Indian equities, may contribute to volatility in the secondary market. The market remains somewhat vulnerable, as direct retail investment has declined. This underscores the importance of renewed FII inflows, which have been absent over the past 12 months, in supporting future market performance.

A weak start to the ongoing Q2 results and muted expectations are the other key fundamental points of concern. However, businesses have started well in the festival season, and expectations have become stronger for a revival in the economy and corporate earnings growth from Q3 onwards. This growth is expected to be sustained in 2026 due to tax reforms. Additionally, the rising probability of Fed rate cuts, progress in Indo-US trade talks, the return of earnings growth and renewed probability of FII inflows are providing tentative support to a positive year-end for 2025.