Over the past one to three months, the Indian stock market has navigated a complex landscape shaped by global economic shifts, geopolitical tensions, downgrades in earnings, FII selling and domestic reforms. The Nifty50 index, a key benchmark, has experienced significant volatility, oscillating between 24,000 and 25,500, reflecting a mix of investor uncertainty and cautious optimism. In the preceding six months, the Indian market could not convincingly trade above 25,000 for any meaningful period. However, this month has witnessed a decisive move past this critical threshold, suggesting a stronger and more sustainable breakout.

A key differentiating factor this time is that domestic reforms, including tax cuts, GST reduction, moderation in inflation and rate cuts, are expected to enhance disposable incomes across both rural and urban households, thereby driving domestic demand. Secondly, the risk regarding US tariffs is reducing, and the market expects at least a mini deal within the next two months. Thirdly, FIIs, who have been significant sellers in the Indian market, are anticipated to return later in the year as the valuation premium gap between India and other emerging markets narrows. Notably, these reforms are expected to support earnings growth from the December quarter onwards, raising optimism that India’s EPS growth could accelerate from the current ~10% level toward 15% in 2026. However, in the near term, the market will have to handle the in-line Q1 expectation on Q2 results and the triple whammy of the 50% tariff, the H1B issue and the Chabahar sanction.

Domestic reforms…

Following the 1,000-points decline in the Nifty50 index in August, an initial rebound was fueled by optimism over potential reforms aimed at stimulating domestic demand. Market sentiment has been supported by the government’s commitment to sustaining economic momentum through measures such as GST rate reductions and targeted sectoral support. However, renewed tariff tensions, particularly the U.S.’s imposition of 50% tariffs on Indian goods, have cast a shadow over the broader outlook. These tariffs, affecting key export sectors such as Textiles, Equipment Manufacturers, Metals, Auto Ancillaries, Seafood, Basmati, and Jewelry, are expected to moderate India’s GDP growth by 50–100 basis points, potentially reducing the projected 7–8% growth to around 6% in the short to medium-term.

Reforms are cancelling the tariff effect

The recent GST rate reductions are expected to stimulate domestic consumption, partially mitigating the adverse impact of lower export competitiveness. Sectors like Durables, Discretionary, Staples, Hotels, FMCG, Electronics, and Autos are poised to benefit. Hence, a loss for a category of sector is replaced by gains for others. India’s economic resilience, highlighted by a strong Q1 GDP, has supported market recovery, although sustainability needs reassessment for Q3. The substantial GST tax cut, estimated at ₹50,000 crore annually, could propel consumption-oriented stocks, which constitute around 18% of the Nifty50, by enhancing their earnings prospects.

Q1 earnings were stimulated with sequential improvement; growth exceeded expectations but stayed muted at around 10%. Mid- and small-cap stocks outperformed their large-cap counterparts, though overall growth continues to lag long-term averages. Corporate earnings growth is projected to stay below historical norms, with FY26 EPS growth forecasted at 10%, challenging current valuations, which remain elevated at a forward P/E of 20.5x.

The market sell-off triggered by the U.S. tariffs saw the Nifty50 drop to 24,400, but optimism surrounding GST rationalization fueled a partial recovery. Given that the U.S. is India’s largest export destination, the impact of these tariffs is likely to become more pronounced from Q3 onwards if they persist. Companies are exploring strategies like cross-country billing and diversified manufacturing to mitigate the impact. Overall, losses are expected to be limited, supported by domestic reforms, including direct tax and GST cuts, alongside moderating inflation and interest rates.

The market expects a drop in tariff issues in the future

A decisive breakout above 25,000 hinges on resolving the U.S.-India trade dispute. Negative narratives from U.S. officials, which had intensified post-tariff implementation, have reversed after the recent diplomatic engagements, including post the SCO Summit, raising hopes for resolution. The market expects that the 50% tariff is unlikely to be a long-term measure, although U.S. trade policy remains uncertain. The markets expects withdrawal of the penalty tariffs and reduction of reciprocal tariff to below 25%.

Despite these global headwinds, the Indian market has shown resilience. The Nifty50 recently surpassed the 25,000 level, which is now seen as a crucial support. This recovery reflects expectations that the domestic impact of U.S. tariffs will be limited, alongside strategic government measures to strengthen India’s geopolitical position. Significant GST reforms have helped cushion short-term economic pressures, and renewed trade talks with the U.S. have further supported market sentiment. However, an increase in H1-B visas is expected to impact the IT sector in the short to medium-term, while in the long term the industry is expected to twist its strong business model accordingly to reverse the negative effect.

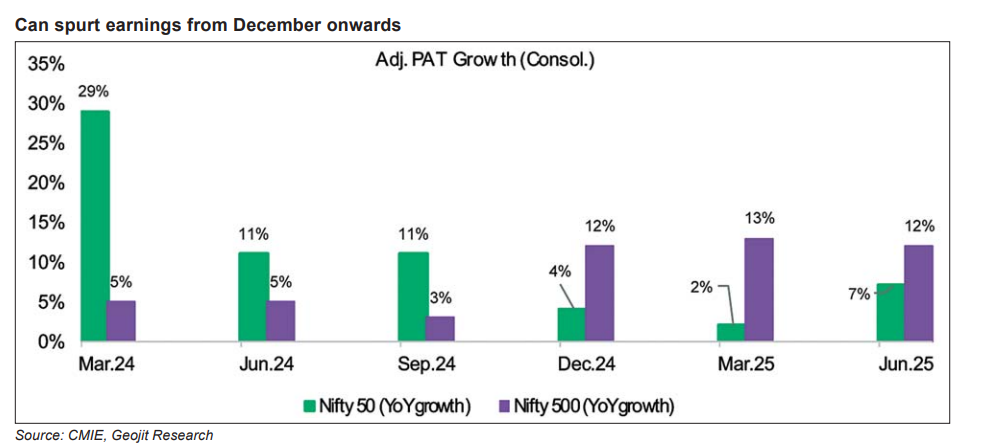

Eyes on the December quarter and FII inflows

For sustained momentum, two factors are critical: accelerated earnings growth and increased FII inflows. While corporate earnings have grown around 10% year-over-year, a sustained rally requires growth closer to 15%. The December quarter is expected to mark the beginning of stronger earnings, driven by tax and GST cuts, increased disposable income, declining inflation, and robust domestic demand. Consumption-based companies, from staples to automotives, are poised for volume and margin expansion, presenting attractive investment opportunities.

Despite these headwinds, DIIs and retail participants have continued to support the equity market, providing a buffer against external volatility. In contrast, FIIs have remained cautious, favoring markets like China over India due to premium valuations and geopolitical considerations with the U.S. Although FIIs have been active in the primary market, their reluctance in the secondary market has influenced India’s performance.

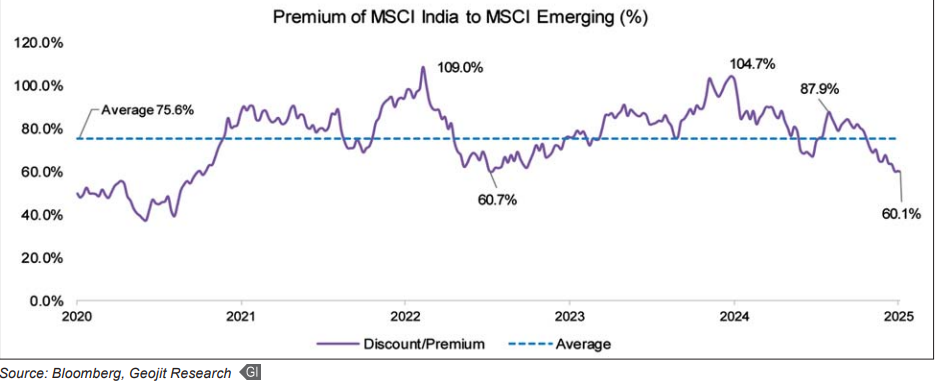

FIIs, who have sold approximately $15.3 billion year-to-date in India’s secondary market, need to shift to being net buyers. Their preference for other Asian and developed markets has been driven by India’s premium valuations and subdued earnings growth. However, expectations of improved earnings from December and a narrowing valuation gap are likely to attract renewed interest. A change in the Fed’s interest rate policy, with anticipated cuts, is expected to weaken the dollar and boost inflows to emerging markets, benefiting India. Market expectations have shifted towards potential Fed rate cuts following weaker job data.

A Drop in India’s Premium Valuation can spur FII inflows in the future