In recent months, Jane Street Group, a US-based proprietary trading giant known for its high-frequency trading (HFT) strategies, has come under intense scrutiny in India. SEBI temporarily barred the firm from participating in the Indian stock market until it deposited its allegedly unlawful gains of Rs. 4,843 crores into an escrow account. This action followed accusations that the group manipulated stock indices through derivative positions.

Let us try to understand what the controversy is about, by starting with something fundamental: arbitrage. Arbitrage, simply put, is when a trader spots a price difference between two related markets and takes advantage of it—buying low in one and selling high in the other. It is supposed to be risk-free and, when done honestly, it strengthens the market.

Let me give you an example. Imagine the Bank Nifty index is trading at 100 rupees. A call option gives you the right to buy it at 90 rupees, and let us say, that option’s premium is 6 rupees. Your total investment is Rs. 96. If you exercise that option and immediately sell at Rs. 100, you make a neat Rs. 4 profit. That is arbitrage using a call option.

But the issue that the SEBI order speaks about is not about legitimate arbitrage. It is about alleged manipulation—about powerful players not just spotting price mismatches but creating them.

Jane Street, according to SEBI, did not merely wait for profitable opportunities. They allegedly engineered them. On expiry days, they would buy index futures and large-cap stocks aggressively in the morning. That drove up the market, making some put options very cheap. So, they bought those puts early. And then, later in the day, they reversed their buying—selling off those positions, dragging the index down. As the market fell, the puts they had purchased earlier suddenly became highly profitable. On paper, it might look like a smart arbitrage trade. But when you cause the price to swing yourself, that is not arbitrage—that’s manipulation.

To understand how this was allegedly executed, it is important to know what kind of firm Jane Street is. A proprietary trading firm, often referred to as a “prop firm,” is a financial organization that uses its own funds to trade stocks, bonds, and other financial assets. Unlike firms that manage client investments or earn commissions, prop firms focus on making profits solely for themselves by leveraging advanced trading techniques and cutting-edge technology.

Jane Street allegedly manipulated the Indian equity derivatives market using four affiliated entities:

- JSI Investments Private Limited

- JSI2 Investments Private Limited

- Jane Street Singapore Private Limited

- Jane Street Asia Trading Limited

These entities were strategically coordinated to execute trades that influenced the Nifty index, especially during closing hours. Jane Street’s entities held large positions in Nifty options and futures. These positions were sensitive to small movements in the Nifty index, especially near expiry. Just before the market closing time, the entities placed large buy/sell orders in Nifty futures. These trades were not economically rational—they were designed to move the index rather than reflect genuine demand and supply. The four entities traded among themselves, creating artificial volume. These trades had no real market risk but gave the illusion of active market interest. This misled other participants and distorted price discovery. The coordinated trades moved the Nifty index just enough to push certain options in-the-money and trigger favourable settlement prices for futures. This resulted in substantial profits for Jane Street’s group. Therefore, SEBI concluded that the trades violated PFUTP Regulations (Prohibition of Fraudulent and Unfair Trade Practices) and Principles of fair market conduct.

Current Status:

On July 21, SEBI issued an update regarding its interim order involving Jane Street Group, stating that the group had met the regulator’s condition by creating an escrow account and depositing Rs. 4,843 crore into it. The account is fully controlled by SEBI, which means Jane Street cannot access or use the funds without SEBI’s authorisation.

SEBI has also directed Jane Street and its affiliated entities to refrain from engaging in fraudulent, manipulative, or unfair trade practices, undertaking any activity that may breach current regulations, using trading patterns identified or alluded to in the interim order. Jane Street has confirmed compliance with these directives.

In addition, stock exchanges have been asked to closely monitor Jane Street’s future trades and positions, ensure the entities do not repeat any manipulative behaviour and maintain vigilance until SEBI’s investigation is complete.

But the question that matters to us most is, what is the impact of the Jane Street saga on trading volumes?

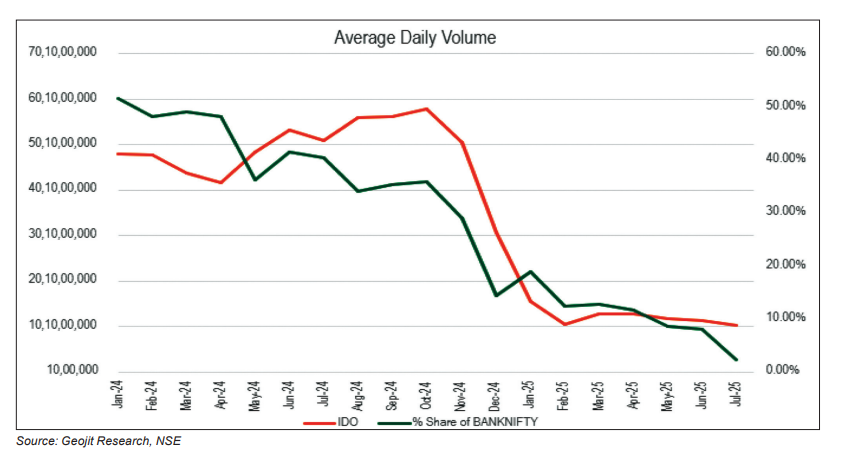

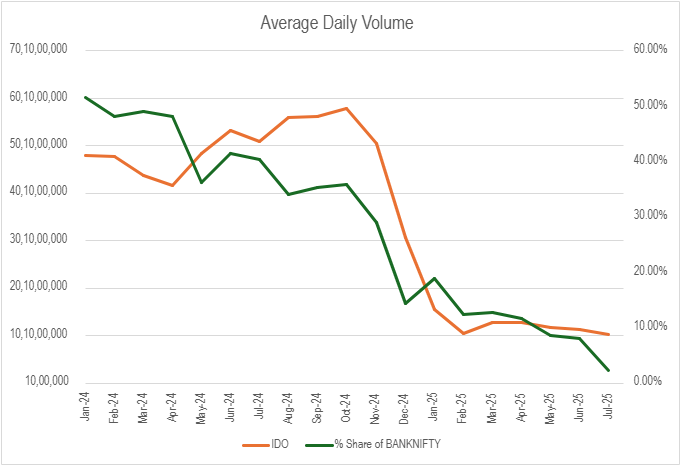

To understand this, we need to look at the influence of HFT traders today in Indian market. They account for about 50-60percent of the trading volume in India’s equity derivatives market. According to Moneycontrol, when NSE issued a caution letter to Jane Street regarding its trades which appeared to be manipulative, it had almost completely stopped trading for two to three weeks. We checked the volumes of February 2025 in NSE, and found that in the first week, the daily average number of contracts traded in the index option segment was 9.8 crores. This in fact rose to 12 crores in the next week, when Jane Street was not present. The figures for the next two weeks were 10.2 and 9.3 crores. This could mean that other high frequency traders probably increased their activity when Jane Street was not there. That said, the number of Bank Nifty contracts traded on NSE in February declined 33percent to 10.47 crores from 15.69 crores in January 2025. Incidentally, SEBI’s interim order noted that Bank Nifty options alone contributed Rs. 17,319.26 crore, amounting to 40 percent of the total Index options profits.

So, what can you expect going forward?

We should certainly expect more vigil from SEBI and exchanges, especially on expiry day volatility and index manipulations. And FPIs could be more cautious with their strategies. Volumes are in fact already down in the first few days of July after the implementation of new derivative rules. In this backdrop, let us not forget that options trading volumes in India declined 70percent in the first five months of 2025 from a year-ago period, as new rules on derivatives made it harder for retail traders to participate.

Geojit Research, NSE

So, what would you choose, a manipulated market, or an illiquid market.

In our view liquidity is very important for all market participants, be it traders, intermediaries, or fin techs. But it is a structural aspect and can be fixed over time. Manipulation strikes at the core of confidence and needs to be addressed immediately.

So, if the large players scale back their volumes, then we could expect lower bid ask along the OTMs. And maybe at least a section of retail traders will stop seeing expiry day as a casino, chasing wild and irrational swings in prices. Or maybe this could pave way for better index construction, as the concentrated weights of some of the stocks in Bank Nifty were one of the aspects helping to move index easily. We believe that markets have a way of self-correcting, over time. But with a 42percent decline in the first 15 days of July, was compared to similar period during June, there is no denying the fact that volumes in the derivative space are on the decline.