Rakesh Agarwal and Melvyn Santarita

Over the weekend, I had an absolute blast watching F1: The Movie, starring Brad Pitt (Sonny Hayes) and Damson Idris (Joshua Pearce). Hans Zimmer’s soaring score only amplified the adrenaline. But amidst the roar of engines and wheel-to-wheel action, one rain-drenched scene during the Italian Grand Prix at Monza struck a deeper chord.

Joshua Pearce, the rookie phenom, chooses to follow veteran Sonny Hayes’s gutsy strategy — staying on dry slick tyres in wet conditions. It works, at first. He flies through the pack and slots into second, right behind Max Verstappen. But ambition gets the better of him. Ignoring Sonny’s advice to wait for the straight, Pearce attempts an overtake in a risky, rain-slick section. Driving at 280 km/h, he brakes a fraction too late. His front tire kisses a wet curb. Grip vanishes. He spins out and slams the barrier.

After the movie, I was reminiscing this scene constantly — It was not just a racing mishap — it was an investing metaphor. Pearce, in that instant, was not just racing Max — he was racing his own expectations. Overconfident in his skill and blind to conditions, he risked everything for the top spot. Investors often behave similarly in bull markets. Flush with recent returns, we often assume the good times will roll on. We chase performance, forget risk, and act like the weather will never change.

But investing, like racing, is not about going fast all the time. It is about knowing when to accelerate — and when to slow down.

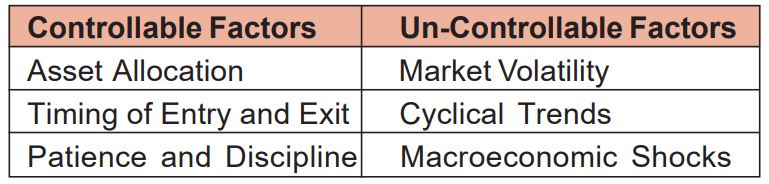

That brings us to a key distinction: knowing what we can control, and what we cannot.

There are aspects of investing entirely in our hands, and others we simply must endure. Great investing is about optimizing what is in your control, and building a framework to act rationally when the uncontrollable kicks in.

This article is obviously not a Nostradamus insight about predicting market tops or bottoms — that’s a fool’s errand. Just like Pearce misjudged the wet curve, many investors misjudge the right moment to make a move. Selling a fund is not about panic or timing the top — it is about responding to the track ahead. Here is a framework that feels more like a pit crew strategy than a formulaic checklist.

- Your Financial Goal Is Approaching- Think of your goal as the checkered flag. If you are nearing, it — whether it is a child’s college or your retirement — the priority shifts from speed to safety. This is when a seasoned team pulls the car in for a tire change, even if the lap times are looking good. In investment terms, that means reducing your equity exposure and rebalancing toward safer instruments like debt or fixed income. It is not exciting, but it is the kind of mature decision that wins races — and secures financial goals.

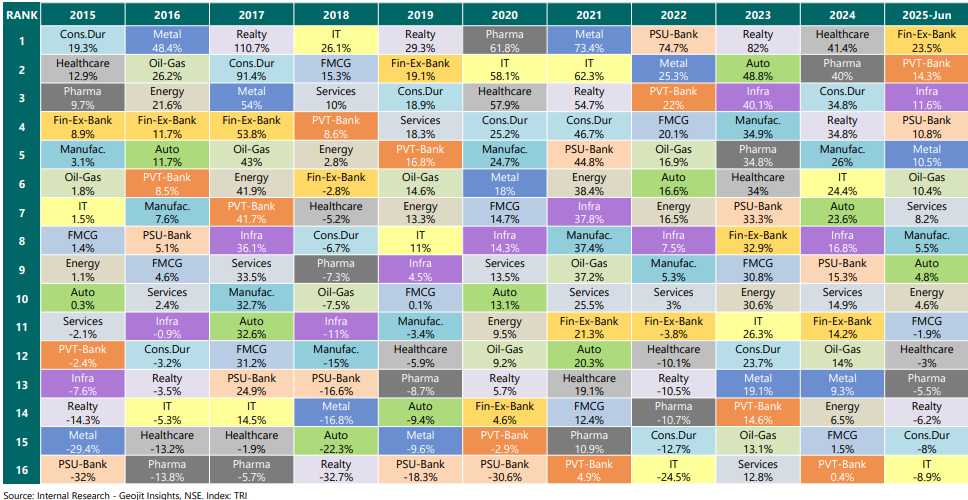

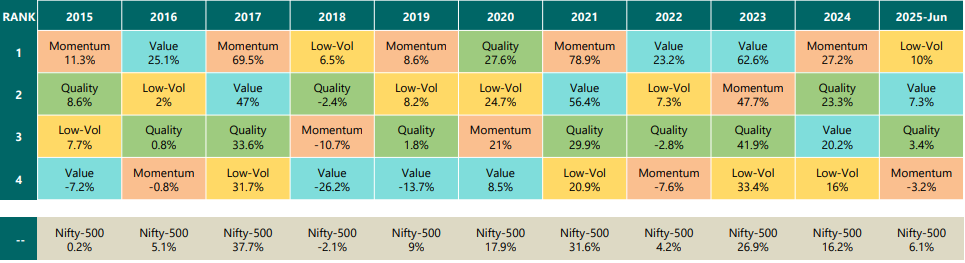

To understand the next 2 conditions, a historical perspective would help a lot coupled with an understanding on market cycles. Markets generally move in cycles both for sectors and styles/factors.

- The Fund Has Outperformed Significantly- Sometimes, a fund delivers well above expectations. That is great — but also a signal to reassess. Is the return sustainable, or has it run too far ahead?

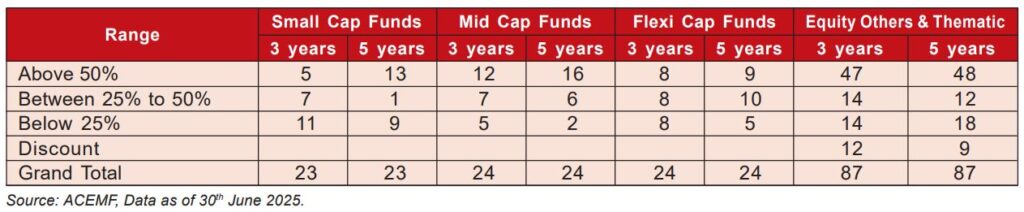

Simply speaking, valuations and returns tend to revert to mean and will not always continue to climb unless there is meaningful re-rating or uptick in the earnings. Just the way we compare the current market P/E to its historical average, we conducted a small exercise to understand the current trailing returns of funds (for 3 years and 5 yrs) compared to its rolling return average over the same period. We then compared them and tried to understand the premium / discount for each fund and tagged them into 4 buckets viz For Premium- “Below 25%”, “Between 25%-50%” and Above 50%, For Discount- Discount depending on what % was their trailing return above the rolling average

The table above helps us understand to what extent are the current returns of the funds above its historical averages. By no means is this a call to sell a fund if they are in a particular bracket – say an “Above 50%” bucket. But it certainly, warrants investors to look if they may need to book some profits and re-align their portfolio by reducing risk. For this study, we considered only those funds for which the 3-year and 5-year rolling data was available.

Our last reason to sell a fund is where definitely a nuanced understanding is required.

- The Fund Has Lost Its Mojo- Not all underperformance is bad. A value-oriented fund lagging in a growth market? That is understandable. But if a fund underperforms even when its style is in favour, then perhaps one needs to dig deeper into understanding its cause.

- Has the fund manager changed?

- Is there a shift in investment strategy?

- Are risk metrics (Sharpe ratio, Standard Deviation, drawdowns) deteriorating?

- Has the fund consistently underperformed across cycles?

While quant numbers (trailing returns) can show a fund in good or bad light. But it is only one element and therefore should never be seen in isolation. To address this, performance must be seen over long time periods and in conjunction with the risk the fund manager took to deliver those returns. Rolling period of performance, batting averages over time periods also give an insight to the ability of the fund manager on his/her execution skills. If there are various datapoints which are seen to be deteriorating or not in alignment with the communicated process framework, then perhaps the fund should be considered for an exit.

The decision to exit a fund should be as difficult as the decision to invest in a fund. I would tend to argue that more focus should be given to which funds are selected to be in an investor’s portfolio. Meticulous screening of processes and fund managers ensures that the funds that make the cut are the ones that have passed through various investment cycles and delivered a consistent return over the cycles and not merely a feast or famine experience. Great portfolios are not made of top performers alone. They are made of complementary performers. You do not need 10 funds doing the same thing. You need a mix:

- Different styles (value, growth, quality)

- Different sizes (large-, mid-, small-cap)

- Low overlap

Once these are identified, then you add the magic ingredient- Patience. Backing fund managers during periods of understandable underperformance is arguably the single most important skill with respect to human behaviour which is frequently tested.

It is our belief that good portfolios are not the ones which have the funds which deliver the best returns. Rather, good portfolios have elements of different styles at all points in time. These portfolios tend to do a good job during bull markets and be resilient during bear markets. This delivers a better experience to investors in the long run.

Although I generally end my note with a cricketing analogy, I was just too blown away by the movie to not end with it. Equity funds, like an F1 car, has the power to hit 300 km/h. But great drivers know it is not just about speed — it is about knowing when to brake, when to pit, and when to let go of a risky move. Sticking to a plan, adjusting for changing conditions, and making unemotional decisions are what get you across the finish line safely. Apex Grand Prix, the fictional team in F1: The Movie, did not have the fastest nor the best car — but it bet on good strategies, experienced insights, and constant review to be the most improved team in the movie. They knew when to take risks and when to pull back. That is the essence of good investing too. Selling a fund is not a sign of failure. It is part of the race strategy. And just like in racing, staying too long on worn-out tires can cost you the podium. Many a times, the smartest move is not to accelerate — it is to exit before the curve. The goal is not to hold forever — it is to hold with purpose and exit with clarity.

Let your portfolio be like Apex — consistent, adaptive, and unshaken by ego or emotion. That is what makes the journey — and the result — truly memorable.