President Trump’s tariff tantrums, which triggered crashes in stock markets globally, have been pushed to the backburner, at least temporarily. The bond market vigilantism forced the Trump administration to beat a hasty retreat from the irrational punitive tariffs declared on 2nd April. The 90-day pause on ‘reciprocal tariffs’, except those imposed on China, calmed the markets. President Trump declared that US would negotiate and strike deals with trading partners. The first such deal was struck between the US and the UK. Then came the temporary agreement with China: The Trump administration drastically reduced the tariffs imposed on China from 145 percent to 30 percent. China, too, followed suit by reducing the tariffs imposed on imports from US from 125 percent to 10 percent. More deals are likely with trading partners in the weeks to come. The much-feared trade war has been averted, at least temporarily. The high level of uncertainty that has been impacting global trade and the global economy has come down.

Global growth will be lower in 2025

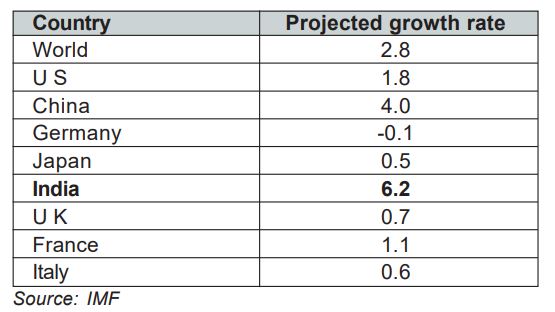

Despite decline in uncertainty, global growth will be lower in 2025.

It is evident that in GDP growth, India would be an outlier with growth above 6 percent, far ahead of the next best growth rate of 4 percent projected for China. If we take the GDP growth rate for FY26, the consensus estimates for India is 6.5 percent.

Global and domestic macros facilitate FII buying

Despite the tensions between India and Pakistan, the market has been exhibiting surprising resilience. The fundamental reason for this resilience has been the sustained FII buying which, in turn, was supported by global macros. FIIs have been big sellers for many months and the big trigger for FII selling since the election of Donald Trump as the US president has been the sharp rise in the dollar index. The spike in the dollar index which peaked at 111 in mid-January 2025 triggered a momentum trade into the US equity and bonds which, in turn, led to massive selling in other markets. FII selling in India in January 2025 was a massive Rs 78,027 crore. With the decline in the dollar index since then FII selling also started declining. FII selling declined to Rs 34,574 crore in February and Rs 3,973 crore in March. President Trump’s reciprocal tariff declaration on 2nd April set alarm bells ringing in global trade and economic circles. The crash in global equity markets following the reciprocal tariff declaration was a clear message that the markets feared a sharp deceleration in global growth in general, and in US and Chinese growth in particular. The consensus that India would remain the fastest growing large economy with above 6 percent growth tilted the scales in favor of India. The RBI initiating a rate cutting cycle with two rate cuts and prospects for more is another shot in the arm for the stock market. Consequently, FIIs turned buyers in India with a net buy figure of Rs 4,223 crore in April. In May, up to 19th FIIs have bought equity for Rs 23,800 crore. This sustained FII buying has imparted resilience to the market. However, it is important to understand that FII flow is ‘hot money’ which can suddenly turn in response to global developments.

The challenge is the revival of earnings growth

The bull run which took the Nifty from the Covid low of 7511 in March 2020 to 26227 in September 2024 was fundamentally supported by earnings growth of above 20 percent CAGR during FY22 to FY24. The sharp correction from the 2024 September peak was triggered by the steep dip in Q2 FY25 GDP growth to 5.6 percent. The sharp dip in earnings growth to 6 percent in FY25 accelerated the market downtrend. If the market rally is to sustain, earnings growth revival is imperative. There are early signs of revenue and earnings recovery: GST collections for April are at a record high of 2.37 lakh crores. The PMI for April is impressive at 58.2 for manufacturing and 58.7 for services. Monsoon has been forecasted to be normal for this year, and this augurs well for food production and food inflation. CPI inflation (3.16 percent in April) remaining well within the RBI’s comfort zone of 4 percent will enable the MPC to cut rates at least twice more in this rate cutting cycle. This will support the stock market.

Trump’s disruptions might continue

Reciprocal tariffs have been paused for 90 days. If trade deals are not struck within this stipulated time, another round of uncertainty might emerge. There can be other Trump threats, too, like those relating to reshoring. Recently, responding to Apple’s plans to significantly scale up Apple’s production from India, Trump said, “Apple should make iPhones in the US, not in India.” In brief, Trump’s MAGA strategy is unlikely to stop with tariffs. President Trump is capable of much more disruptions.