Between 27 September 2024, and 07 April 2025, India’s broader market witnessed a significant correction of 21%. This decline came on the heels of a sharp postelection rally sparked by the incumbent government’s third consecutive term. The rally propelled India’s market capitalisation to $4.8 trillion and drove the market cap-to-GDP ratio to 145% – substantially higher than the 10 year average of around 90%. Simultaneously, corporate earnings for FY25 fell short of expectations, triggering a valuation-driven market consolidation. Over a period, the projected earnings growth for Nifty 50 was revised down from 12% YoY to just 5%, reflecting a challenging macroeconomic environment. Contributing factors included reduced government expenditure amid frequent election cycles, subdued rural and urban demand due to erratic monsoons and elevated inflation, and global pressures that squeezed profit margins. Mid and smallcap segments bore the brunt of the downturn, with the Nifty MidSmallcap 400 Index plunging by as much as 25% intraday during the same period.

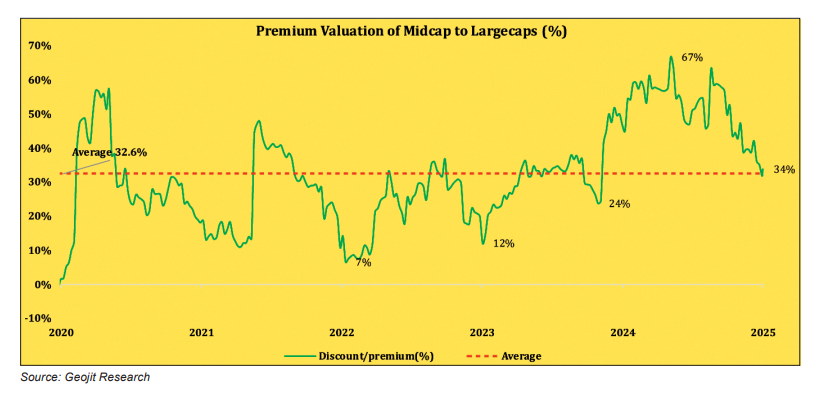

Encouragingly, the ongoing Q4FY25 earnings show signs of recovery, with Nifty 500 companies reporting 10.5% growth, outpacing large caps. This rebound is being supported by declining wholesale inflation (WPI at 0.85% in April), which is softening input costs, thus restoring operating margins. The outlook for FY26 is optimistic, supported by easing inflation and interest rates, rising disposable income due to indirect tax relief, and a likely boost in government spending following the general elections. Global risks are also easing, with reduced geopolitical tensions and fading US recession fears. Valuations have become more soothing, with the midcap premium to large caps normalizing to 34% from a peak of 67%, close to the five-year average of 33%. With earnings momentum picking up and macroeconomic fundamentals turning more supportive, mid and smallcap segments are increasingly well-positioned for a mediumterm rebound.

Reduction in domestic risk

For mid and smallcap stocks to maintain a healthy trading trajectory, a balanced risk environment across the economy and financial markets is essential. Such conditions generally prevail when both political and economic landscapes exhibit stability. Currently, such stability is evident in the domestic market, supported by factors like the ceasefire between India and Pakistan, a significant decline in inflation, anticipated interest rate cuts, and a stable government. Such conditions contribute to a more predictable and secure business climate, effectively reducing the country’s overall risk profile. In equity markets, this translates into heightened investor risk appetite, often resulting in the outperformance of midcap stocks. Additionally, the environment creates arbitrage opportunities; for instance, investors may capitalize on lower borrowing costs in anticipation of further improvements in market sentiment, driven by a strengthening business outlook.

Investors often gravitate towards riskier assets such as mid and smallcap stocks in pursuit of higher returns. In India, midcaps particularly perform well due to their stronger revenue and earnings growth potential, supported by their ability to capitalize on emerging opportunities leading to higher growth and a low base. In the last five years, the Nifty Midcap150 Index has provided an absolute return of 330% versus 172% of the Nifty 50; YTD is -2.2% and 5.2%, respectively.

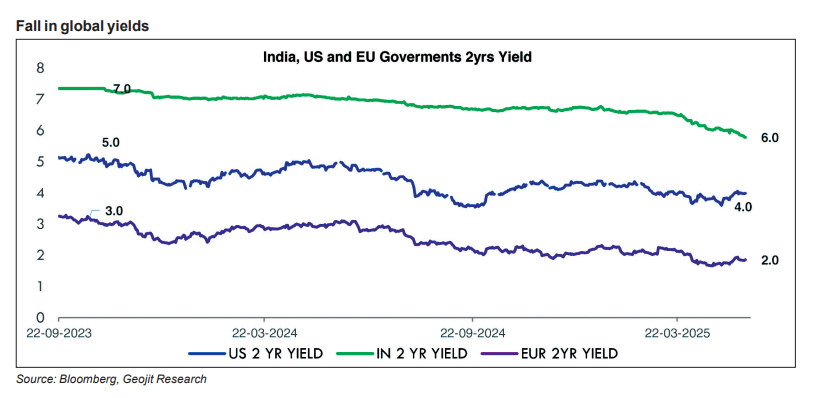

Signs of reduction in global risk too

A comparable trend is unfolding in global markets. Although the European Union is weighing new sanctions against Russia, prospects for a ceasefire with Ukraine remain high on the horizon. Importantly, the world’s biggest risk was the tariff war, which is diminishing following the pause of reciprocal tariffs. At the same time, many countries are entering into Free Trade Agreements (FTAs), which are expected to stabilize future trade uncertainties.

Global interest rates are on a downward trajectory, signalling a moderation in financial risks. However, this decline also reflects a slowdown in economic growth, pointing to potential contraction and an increase in economic risk. That said, fears of a global recession have been easing in recent months, contributing to a more favourable outlook for equity markets. This evolving landscape is poised to enhance the stock market’s riskreward profile, supported by a mix of more attractive valuations and falling bond yields. This is expected to bolster corporate earnings while encouraging renewed capital inflows into emerging markets.

Chance of revamp in inflows

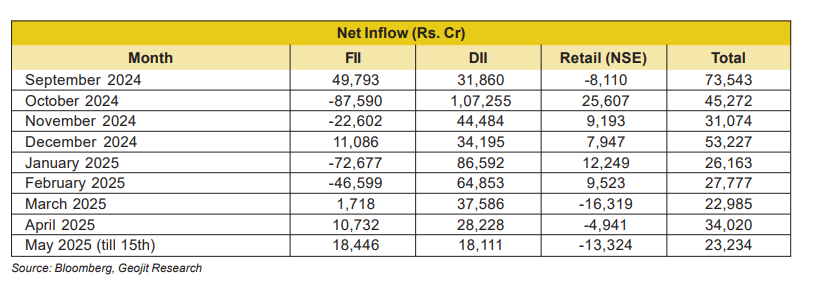

With rising risk appetite, a resurgence in capital inflows appears likely. FIIs have cautiously started returning to Indian markets, with marginally positive inflows recorded since April. However, a sustained and decisive uptick will depend on a broader shift in global investor sentiment – from a risk-off to a risk-on stance. Currently, FIIs’ concerns remain largely concentrated on the US market, which has inflationary risk from the potential tariff increases and a low probability of FED rate cuts. Many US companies are signalling potential price hikes for the consumers. Simultaneously, President Trump is introducing tax cuts, creating a mixed outlook that while these cuts may boost corporate earnings, it will also widen the already elevated fiscal deficit.

The recent easing of trade tensions between the US and China is expected to benefit other Asian economies more than India in the short term due to a change in perception. However, over the longer term, India is wellpositioned to capitalize on the global realignment of supply chains, emerging as a strategic alternative manufacturing hub. While FII flows may temporarily shift to other markets, India continues to hold strong as a long-term investment destination.

Domestic Institutional Investors (DIIs) have maintained a steady pace of investment in the markets, though their intensity has slightly eased in response to the recent pickup in FII inflows. Meanwhile, retail investors appear to be in a profit-booking phase following substantial buying activity between October 2024 and February 2025. However, this trend is expected to reverse as broader market sentiment strengthens in the coming months.

Earnings growth looking at Q1FY26

Stronger-than-expected Q4 results have sparked optimism for the upcoming quarters. The Nifty 500 index companies reported a PAT growth of 10.5%, while the Nifty 50 index posted an 8% increase – both hugely outperforming the weak estimates of zero growth. Notably, the broader market appears to have outperformed the benchmark indices, signalling a meaningful uptick in earnings from mid and smallcap companies.

The prevailing market consensus indicates that following a muted FY25, India’s EPS growth is projected to recover to 10-12% in FY26 from the current estimate of around 5%. If mid and smallcap companies continue to deliver strong performance – as indicated by Q4 trends – it

could significantly improve sentiment toward these segments. As a result, Q1 earnings data will be critical in sustaining and further building this optimism.

Drop in midcap premiumisation

The valuation premium of Indian midcap stocks has contracted sharply during the recent market consolidation, falling from a peak of 67% to 34%, now nearly in line with the five-year average of 33%. This reversion signals a potentially attractive entry point for long-term investors to accumulate. If earnings growth surprises on the upside in the coming quarters, midcaps could be well-positioned for a period of outperformance.

Sectors to vouch for

Several macroeconomic and policy-driven factors are aligning to create a favourable environment for Indian equities:

• Rising disposable incomes: The tax cuts announced in the 2025-26 Union Budget are expected to boost household spending power.

• Falling inflation: Lower input costs are improving corporate margins, especially in manufacturing and consumption-linked sectors.

• Increased government spending: Post-election fiscal activity is gaining momentum, particularly in infrastructure and capital expenditure.

• Declining interest rates: Easing rates are expected to lower borrowing costs, spurring both consumer demand and corporate investments.

Amid these supportive tailwinds, rate-sensitive sectors such as Finance, Auto, Real Estate, and Consumer Durables appear well-positioned for growth. Additionally, Infrastructure, Equipment Manufacturers (valuations are on the higher side), and Cement sectors are likely to benefit from increased government spending.

The Textile sector is emerging as a standout performer, supported by favourable trade dynamics – like lower[1]than-expected tariffs on India, high tariffs on competitors and weakening competitiveness from key exporters like China and Bangladesh (political instability and economic impositions by India on Bangladesh) are creating opportunities for domestic textile players. FMCG also looks bright in anticipation of a good monsoon, reduction in inflation, improvement in rural and urban demand, and reasonable valuations.

From a valuation perspective, most of these sectors are trading at relatively sober levels compared to their 5-year averages. The broader Indian market is currently valued at around 20x one-year forward P/E, which is about 5% above the 5-year average – a level that still leaves room for upside, especially if earnings momentum picks up. Preliminary indicators suggest the potential for upward earnings revisions. Should earnings trend toward 15% EPS growth, it could spark a broader market rally. In this context, the upcoming Q1 results will be pivotal, potentially serving as a catalyst for further re-rating across sectors.