Many economists think that the current financial landscape with escalating trade tensions and heightened market volatility creates the risk of recession in the U.S. However, despite these challenges, India’s corporate sector and financial markets have demonstrated notable resilience. Although the primary market has seen a temporary decline in fresh issues, strong corporate balance sheets and sustained capital inflows over the past few years have limited the need for immediate funding.

The long-term outlook for Indian equities remains positive, even as short- to medium-term headwinds persist due to external risks. A strategic diversification across asset classes—combining equities, debt instruments, and safe-haven assets like gold—is recommended for investors to navigate this volatile environment. New investors, in particular, are encouraged to adopt systematic investment approaches and focus on domestically driven sectors such as consumption, infrastructure, and financial services.

Corporate earnings for Q4FY25 are expected to show sequential improvement but will likely reflect muted YoY growth due to a high base effect. The outlook for FY26 has been cautiously revised downward, considering the external factors. Sectors such as IT and export-driven industries face pressure, while domestically oriented industries are positioned to perform relatively better. India’s ongoing trade negotiations and strategic sectoral strengths offer it a unique opportunity to strengthen its global economic standing.

India’s financial resilience, proactive policy engagements, and internal economic momentum position it favourably amid global uncertainty. For investors, a disciplined, diversified strategy remains critical in converting today’s volatility into long-term opportunity.

India’s financial resilience amid global trade turmoil

As global trade uncertainty deepens and market volatility surges, India’s corporate sector and financial markets have shown remarkable resilience. While fresh issuances in the primary market have temporarily dried up, many companies are expected to line up to get listed or do Qualified Institutional Placement (QIP) during the year. The impact of the ongoing slowdown in funding on the broader market is forecast to be muted. Significant capital was raised over the past few years, which has strengthened corporate balance sheets, supporting ongoing capital expenditure plans.

Despite global headwinds, India’s fiscal and corporate foundations are solid. A revival in the primary market is expected as investor sentiment improves, which hinges largely on stabilization in global trade policies and cuts in interest rates. Even with the ongoing friction between the US and China, India’s comparatively stable stance on tariffs and trade agreements bodes well for sustaining investor confidence. It is even expected that the trade war between the world’s two largest economies will benefit India in the long term.

Global trade tensions: Storm clouds or silver linings?

The announcement of reciprocal tariffs by the US in early April 2025 sent shockwaves across global equity markets, causing a sharp correction. Markets breathed a sigh of relief after the US administration paused tariff implementation for most countries, excluding China. Nevertheless, escalating trade tensions between the US and China continue to threaten global economic stability.

For India, the evolving trade dynamics present both challenges and opportunities. Bilateral negotiations with the US could yield favourable outcomes, helping India shield itself from the worst of global disruptions. India is in discussion with other nations like the UK and the EU for an FTA to bring further stability in the future. Furthermore, India’s measured and constructive approach toward trade diversification offers new avenues for growth, particularly in manufacturing and services. The US has started discussing many trade patterns to finalise a deal, indicating that the worst regarding the trade war is behind us. On that note, the market is on a sharp recovery trend presuming that the worst is factored in. The last low made by the domestic market on 7th April is expected to stay protected given the improvement in trade tactics.

A rising risk of recession

The probability of a US recession has surged during the year as trade tensions heighten economic risks. The reciprocal tariff has been capped at 10%, lowering the feared impact. However, the heightened trade war between the US and China, is expected to increase inflation and slow the world economy.

Another consideration is that the interest rate in the US still remains elevated at 4.5%. The FED is not in a position to cut rates due to the uncertainty brought about by Trump’s trade policy. However, with the peak of the trade war now deferred in anticipation of future agreements, there is a positive outlook for potential rate cuts by the Fed. Meanwhile, the ECB has implemented its seventh consecutive rate cut, bringing it down to 2.25% in response to economic slowdown concerns. This move is expected to mitigate recession risks in the EU. Similarly, other major economies such as India and China are adopting liquidity-supportive measures to bolster their domestic economies.

India’s domestic strength: A beacon in volatile times

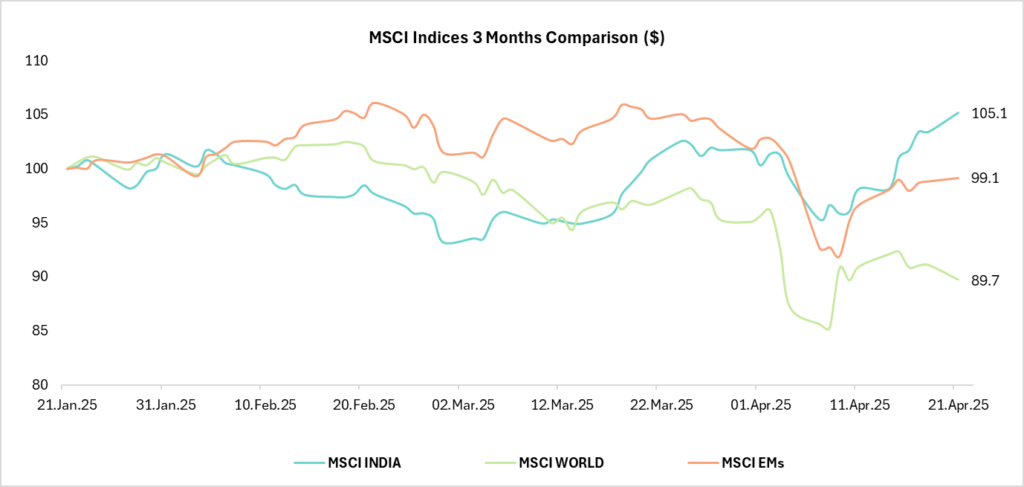

Outperformance of India to the world

Source: Geojit Research

Though India is better positioned than many of its peers, it cannot remain completely insulated. A global slowdown would inevitably affect demand, investments, and market sentiment. Thus, cautious optimism and strategic flexibility are the needs of the hour for Indian investors and businesses alike. Despite the global turbulence, India’s financial markets are holding relatively steady. The limited correction witnessed domestically during the global sell-off underscores India’s internal resilience. Forward-looking indicators such as the index of industrial production (IIP) and PMI suggest that India’s economic momentum remains intact. The upcoming Q4 earnings season will be critical in reaffirming this momentum. While sequential improvement is expected, the YoY earnings growth may be modest, capping substantial improvement in market sentiment. However, since the latest correction was triggered by a global sell-off, it is highly possible that the muted Q4 may not have a deep effect on the market trend. The market will likely focus on FY26 earnings outlook, presuming that FY25 is behind us.

Corporate earnings: A subdued but stable picture

The corporate earnings season for Q4FY25 is expected to show sequential improvement over Q3, supported by government spending and positive economic indicators. However, YoY growth may appear subdued due to a high base effect from the previous fiscal year.

Given the current global backdrop, earnings growth forecasts for FY26 have been trimmed. Reciprocal tariffs introduced in April, along with rising recession risks, are likely to dampen corporate performance. Although optimism persists, cautious realism is warranted as global trade disruptions may weigh on earnings further into the next financial year Simultaneously, valuations have corrected to long-term averages, reflecting that further correction is buying opportunity for long-term investors; otherwise, accumulation is warranted in a staggered buying method. We are maintaining 12-14% YoY growth for India EPS in FY26, led by buoyant domestic demand, rate cuts and reduction in inflation.

For new investors: A strategic starting point

The current market chaos presents an excellent opportunity for first-time investors to lay a strong foundation for wealth creation. Understanding the cyclical nature of equity markets—shaped by global, domestic, and company-specific factors—is essential. A systematic approach via direct equity SIPs can smoothen the volatile entry point. New investors should focus on domestically oriented sectors such as FMCG, discretionary consumption, infrastructure, cement, telecom, and financial services, targeting sector-leading companies. A balanced portfolio, with around 30–40% allocated to high-quality debt instruments, can provide steady income while mitigating portfolio volatility.

The market outlook: Long-term optimistic

A long-term positive outlook persists for Indian equities, although the short- to medium-term may reflect turbulence. The world is currently grappling with economic tightening and trade disruptions, factors that may temper growth. Nevertheless, India’s focus on strengthening manufacturing capabilities and expanding its share in global trade places it on a steady trajectory. In today’s volatile environment, diversification across asset classes remains crucial. A strategy that combines debt instruments, safe-haven assets like gold, and select domestic cyclical sectors offers investors a robust way to manage risk while capturing future growth opportunities. After the deep fall of the last seven months the prices of many mid and small caps have become attractive. However, given the uncertainty in the short-term it is advised to hold a multi cap approach with importance to large caps for the time being.

Sector winners and losers: A mixed bag

India’s resilience does not imply immunity. Sectors heavily dependent on U.S. exports are facing headwinds. The subdued technology spending is crimping growth prospects for Indian IT firms, many of which derive a significant portion of their revenue from American clients. Similarly, export-driven industries such as pharma, auto ancillaries, textiles, and aquaculture are exposed to the ongoing trade turbulence. At the same time, such companies’ valuations have become attractive for long-term investors to start investing in them. Notably, exemptions from tariffs for sectors like pharma, semiconductors, and energy-related commodities offer a cushion, positioning India’s players favourably against global peers. Conversely, domestic-oriented sectors such as agriculture, FMCG, consumer oriented, financial services, infrastructure, and cement are expected to outperform, benefiting from limited direct exposure to global trade conflicts and stable domestic demand.

2 comments

Very crisp write up – No, not a mere write-up, it’s distilled essence of the present – by Vinod Nair.

Thanks to Geojit for disseminatiing this !

It was a good analysis of world happenings and have given comfort on Indian market

Mudit

BBK NRI