The US stock market, the undisputed leader in global financial landscape, is facing a decline due to policy uncertainties under the Trump administration. The best-performing stock market, the US is now facing ambiguity due to evolving international trade policies and deficit-control measures. These factors have raised concerns about a potential economic slowdown, with some even speculating about a recession in a year, though such predictions remain premature. Lately, S&P 500 and Nasdaq 100 had corrections of 10% and 14% on an intraday high & low basis.

Interestingly, the Indian stock market is demonstrating notable resilience despite being in a corrective phase since September 2024. Its recent outperformance has been driven by a decline in the US Dollar Index (DXY), which traditionally shares an inverse relationship with emerging markets over the long term. A significant drop in the DXY signals potential weakness in the US economy, benefiting markets like India.

Additionally, the upturn of the domestic stock market is also supported by improvements in domestic economic factors like the fall in inflation, improvement in IIP and PMI data, and interest rate cut scenarios. Market sentiment is gradually strengthening, with projections suggesting that earnings growth in India could improve from Q4FY25 onwards, potentially rebounding toward the long-term average of 15%. If this materializes, it will be further reinforced by government efforts to boost disposable income for households, which could drive increased consumer demand and fuel stock market growth in FY26.

The weakness of the US market…

The Trump administration has introduced significant shifts in the US approach to international policy, distancing itself from key global agreements and organizations such as the WTO, the Paris Agreement, NATO and the WHO. This departure has disrupted the established global order that prevailed until 2024, leading to increasing tensions between nations and casting uncertainty over the US economic outlook. Concerns are growing that these policy changes could contribute to a slowdown in the global economy and a potential recession in the US. Trade disputes have started between the US, on one side, and China, Canada, Mexico and the EU, on the other, which can impact the US economy too.

This time, policymakers anticipate a short-term increase in economic disruption but are willing to endure temporary losses for long-term gains. They believe these measures will lead to structural reforms that help control the fiscal deficit. The CY24 fiscal deficit is at 6.5%, and the new government target is to bring it down to 3.5%.

Until a month ago, the strong performance of the US stock market was driven by the consistent rise of the DXY. This increase was fuelled by expectations of a slowdown in emerging economies, a reversal of capital flows toward the more stable US market, and the effects of quantitative tightening. But now the persistent high Fed rate of 4.5%, compared to 2.5% in the EU and new policies are likely to impact the US economy. For example, a 25% tariff on Steel and Aluminium is increasing metal prices in America. Going forward, the deployment of reciprocal tariffs is increasing uncertainty about global trade, and the US is expected to lose more than gain by increasing tariffs.

As a result, the US stock market, which was the best performer and the last course of resort, has weakened over the last month. The S&P and Nasdaq corrected by 10% and 14% from the recent high to the low. This situation is expected to stay tight unless clarity emerges about tariff policy, international policies, rate cuts, and economic growth. The one-year forward P/E valuation of the US has come down from 24x to 20.5x, but it is still on the higher side.

Global investors’ growing apprehension is that a prolonged downturn in the US market could have a ripple effect on the entire world markets, potentially spilling over to the world stock market. And the standoff involving key economies, the US, Europe and China, heightened the risks of slowing down the world economy. Fortunately, India remains largely insulated from these disruptions with low goods trade and high services exports. However, goods exports are expected to rise in the future and the government is working to finalize the FTA deal with the US to support the case.

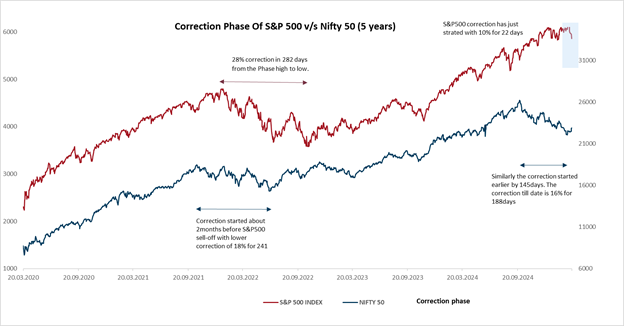

Pattern between S&P500 and Nifty50

The resilience of India…

In the wake of the US market correction, EMs are seeing increased inflows, with China being the primary beneficiary. This trend is driven by the inverse relationship between the DXY and EMs, as the declining dollar value has led to increased capital inflows in these markets. The Chinese market is up by 20% in the last 3 months as the best performer. Supportive measures to stimulate the economy, excitement in IT stocks over AI development (DeepSeek), extending friendly hands to the private players to boost the economy and cheap valuation of 11x P/E (Hang Seng Index) are speeding the Chinese market. Meanwhile, developed European markets are also showing resilience, benefiting from rising defence spending and liquidity measures by the ECB, which recently reduced its key interest rate from 4.5% to 2.5%.

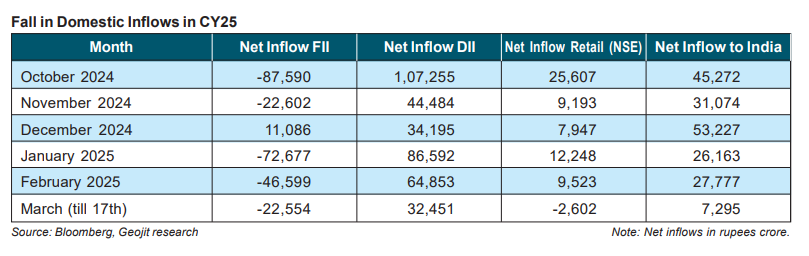

Between September and December 2024, despite heavy FII selling, the Indian market remained resilient, supported by strong buying from mutual funds and retail investors. However, from January to March, continued weakness in both global and domestic markets weighed on investor sentiment, leading to a decline in inflows and a 20% drop in the broader market.

India joined the EMs rally on a late note by the second half of March, as FIIs continued to sell, and domestic inflows stayed low. Consistent improvement in Europe and EMs along with rapid recovery in domestic economic data boosted the domestic market from the oversold level.

March is historically a good month for India. Improvement in IIP, PMI and reduction in inflation and crude data have boosted sentiment. RBI is expected to make the second 25bps cut in April, and more is expected in the future. Optimism is emerging that earnings growth will improve in FY26. If the growth moves towards the long-term average of 15%, we can expect the momentum to shift to bullish. In the near term, volatility may rise based on the development of whether the reciprocal tariff will be implemented in April. However, this is expected to be addressed through a bilateral trade agreement that is currently in its final stages of negotiation.

Sectors which can gain

The rate cut scenario is expected to benefit rate-sensitive sectors such as banking, NBFCs, auto, consumer durables, and real estate. Lower interest rates reduce borrowing costs, which can boost demand for loans and improve profitability for banks and NBFCs. Similarly, the auto, real estate, and consumer durables sectors benefit from increased consumer affordability due to lower loan rates. This presents an attractive opportunity for investors to consider rate-sensitive stocks, as they are still in the early stages of the rate cut cycle. Following the broad market correction, most sectors have seen a sharp decline in valuations, with many reverting to or even falling below their long-term averages. Among these, certain sectors like banking have valuations near -1 standard deviation of their long-term valuation, making them particularly attractive for investors.

From a long-term perspective, India has been the best-performing emerging market over the past five years, with MSCI India delivering a 22% CAGR in the last 5 years. However, in the short term, it has been one of the weakest performers as FIIs continue to book profits. The current impact is more pronounced in sectors and stocks where earnings growth is below the long-term average, due to short-term disruption. This has created an opportunity for long-term investors. Looking ahead, the pace of earnings downgrades is expected to ease, supported by increased government spending, lower interest rates, and tax reductions. These factors are likely to provide a boost to sectors such as FMCG, consumer discretionary, banking and chemicals, which are trading at fair valuation today.