Market cycles synopsis

Markets and valuations tend to mean-revert, a trend evident in Indian equities’ historical cycles. Between 2002 and 2007, the Nifty index multiplied sixfold, driven by global demand, margin expansion, robust topline growth (25%+ CAGR), capex, credit growth, and high ROE. This demand-led bull market was replicated globally as well.

But from 2007 to 2013, markets remained flat, followed by a 2x return between 2013 and 2019. Post-COVID, we are again in a bull market phase, but with notable valuation concerns. Current valuations when compared to the long-term historical averages seem stretched, with Market Cap to GDP at 136%, P/B ratio at 4.4x, and P/E ratio at 22.7. Historically, when P/B exceeds 4x,returns tend to normalize or stagnate from a mediumterm perspective. Only India, the USA (Big Tech), and Japan have delivered strong returns globally postCOVID. Indian markets have been driven by supply-side distortions and government spending on capital projects. Yet, these supply shocks usually stabilize in a few quarters, and the temporary spike in demand diminishes swiftly, resulting in short-lived sectoral booms.

Examples include

• IT (2020, digitization theme)

• Metals and Speciality chemicals (China+1)

• Consumer durables and banking (2021 & 2022)

• Recent focus on capex and auto sectors (2023-2024)

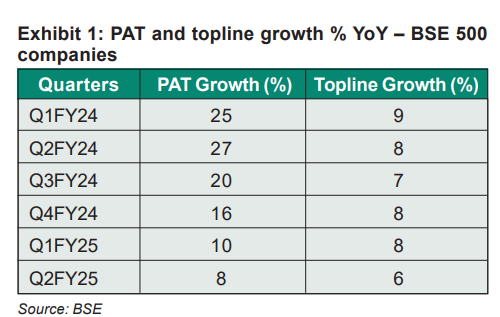

Convergence in PAT and topline growth for BSE 500 signals a cyclical slowdown, with earnings cuts visible across sectors. There are sectors where margins have already peaked. While the long-term prospects for Indian equities are strong, the present conditions require careful selection of instruments and allocations to prevent capital destruction.

Strategic investment approach: Multi-asset category

Cricket is an engaging way to illustrate investment philosophies. The three game formats—T20, ODI, and Test—demand different skill sets and approaches. While a player can excel in all three, their strategy must adapt: T20 requires aggressive hitting, while Test matches call for patience. A skilled all-rounder, though not the top batsman or bowler, plays a crucial role in a team’s success.

In investing, balancing growth opportunities with higher risks is vital. Investors should consider diversifying their portfolios with various asset classes for superior riskadjusted returns. The Multi-Asset Fund category is an effective option for achieving strong financial performance and reaching your investment goals.

Multi-asset funds: Approach and objectives

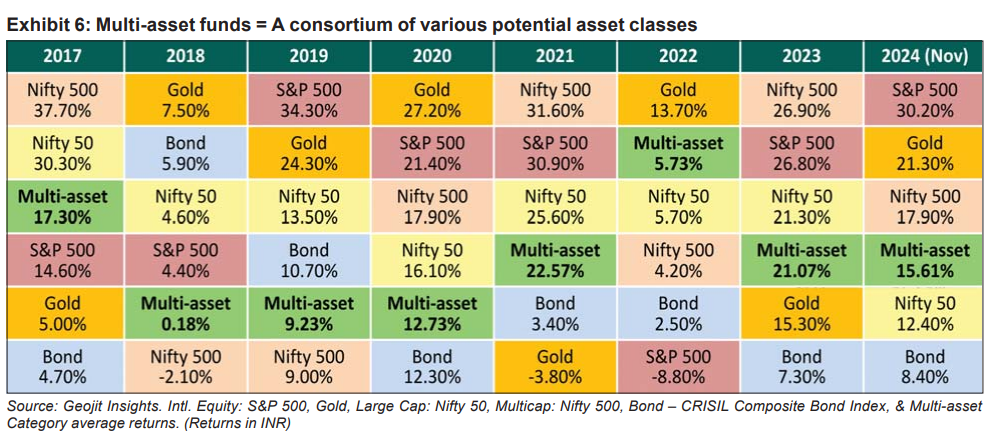

At their core, funds in this category typically diversify their assets across equities, fixed income, and precious metals. Regulations require these funds to allocate at least 10% of their assets to each of these classes. However, many funds have broadened their scope to include additional asset classes as well.

Swiss Army Knife Approach

• Equity: Capital appreciation

• Fixed Income: Aims to offer accrual returns

• Precious Metals: Hedge against inflation

• REITs/InvITs/Arbitrage: Yield enhancement strategies

A multi-asset fund is a versatile addition to your investment portfolio. It aims to generate superior riskadjusted returns by adding various potential asset classes. Typically, these funds allocate resources across large-cap, mid-cap, and small-cap equities, with some offering international exposure for enhanced diversification.

Incorporating fixed income, Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), and precious metals like gold and silver adds stability during market fluctuations and aims for consistent returns.

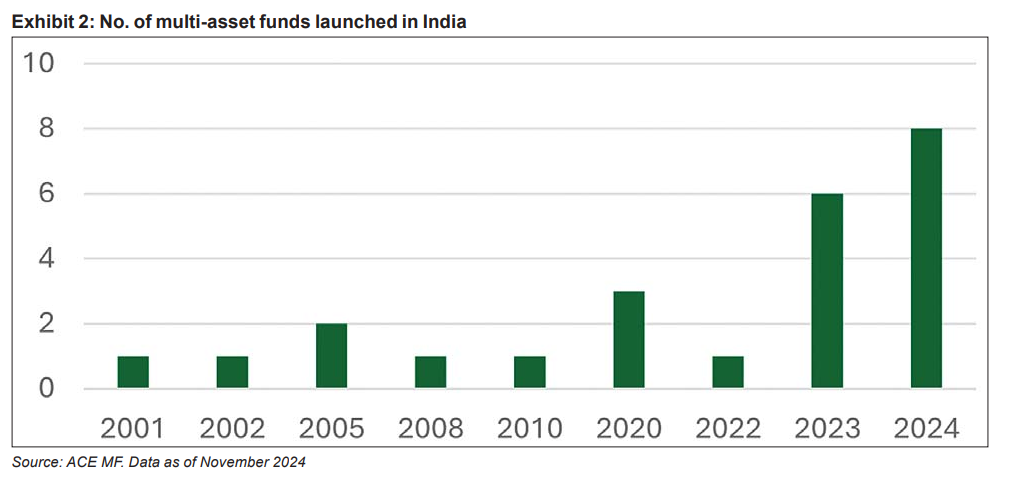

Many funds in this category allocate around 65% to equities, 20%-25% to fixed income, and 10%-15% to precious metals. With the rising popularity of multi-asset funds demonstrated by a surge in new launches, now is a great time to consider them for your portfolio.

As investors and advisors, we recognize that evaluating a fund solely based on its returns can be short-sighted.

It is crucial to assess the returns in relation to the risks taken to achieve them. We aim to support the case for a multi-asset fund through the lens of W. Edwards Deming’s famous quote: “In God we trust; all others must bring data.”

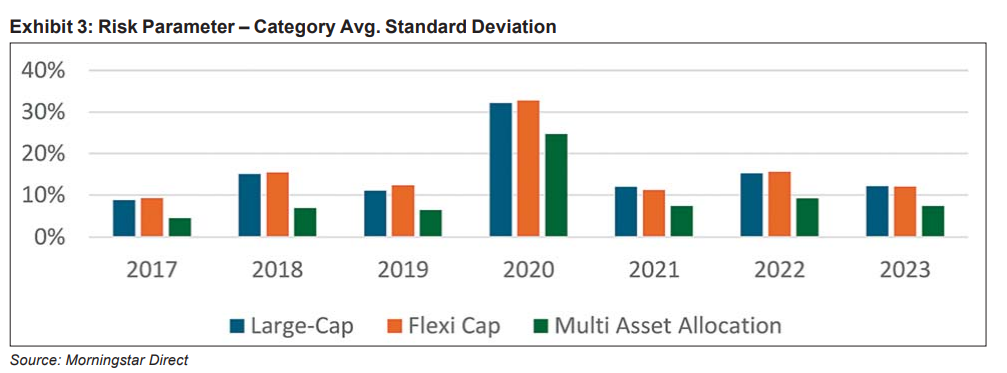

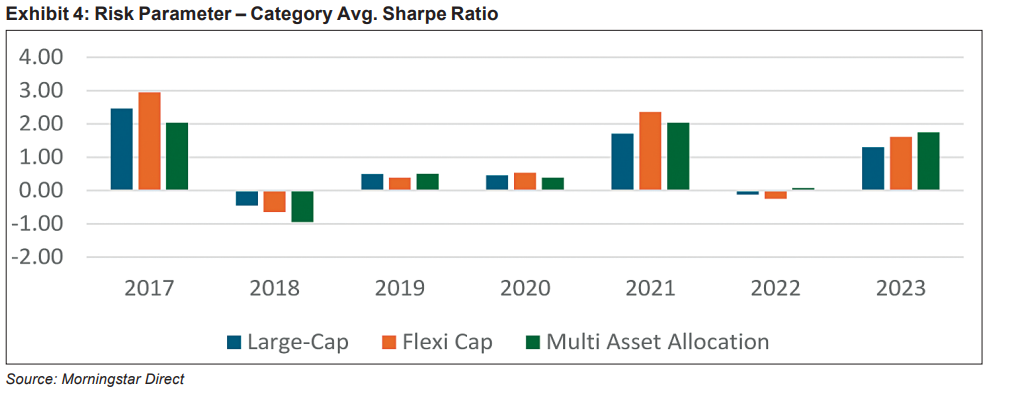

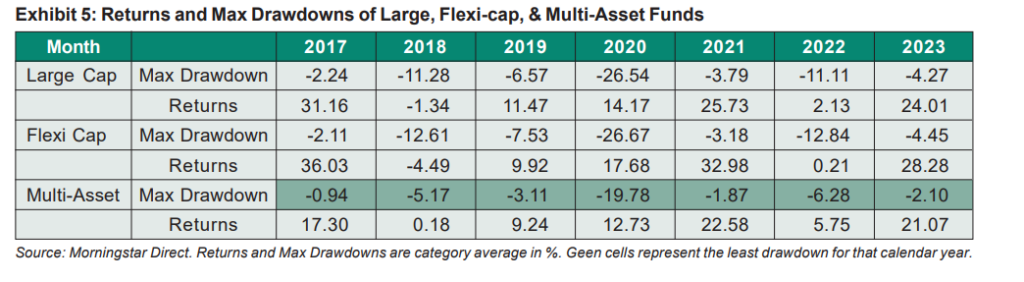

The charts presented below clearly illustrate that a multiasset fund can manage large drawdowns during volatile periods and yet capture a significant upside during market recoveries. Its allocation across asset classes helps to generate favorable risk-adjusted returns (Higher Sharpe & Lower Standard Deviation) vis-à-vis a pure play Large or Flexi-cap category.

Multi-asset funds: Returns vs risk

Asset allocation: The secret sauce! When it comes to investment returns, multi-asset funds are not designed to consistently outperform pure equity funds over the long term. However, they excel at managing risk and delivering respectable risk-adjusted returns. This is achieved by cushioning the portfolio during volatile periods and capturing a reasonable portion of the upside during market bull runs. As illustrated in the table below, markets go through cycles, and in this context, multi-asset funds have shown impressive performance each year by providing strong risk-adjusted returns.

Three important considerations when investing in multi-asset funds:

1. Complement, not a replacement: Multi-asset funds are designed to complement your core asset allocation, which should still include diversified equity funds like large-cap, flexi-cap, and multi-cap funds. They should not replace these core investments.

2. Long-term investment: Investing in equities is typically a long-term strategy, and this holds for multiasset funds as well. While these funds are allocated to different asset classes to help reduce risk, they tend to yield the best returns when the investment horizon is at least three years or more.

3. Unique offerings: Each multi-asset fund is unique, so it’s essential to consult with your financial advisor or conduct thorough research to determine the suitability of a specific fund for your portfolio. Understand the taxation applicable to your fund selected based on equity allocation.