India macro synopsis

As of October 2024, the Indian economy remains stable, with Manufacturing and Services PMI at 57.5 percent and 58.5 percent, respectively. Gross fixed capital formation as a percent of GDP has been on an increasing trend since FY21. The Reserve Bank of India maintains its GDP growth forecast at 7.2 percent year-on-year, despite increases in CPI and core inflation to 5.5 percent and 3.6 percent respectively. The RBI’s shift to a ‘neutral’ policy stance may allow for interest rate cuts in 2025. Reviving government capital expenditure is crucial in 2HFY25 caused by slower growth in the first half due to elections and monsoon effects.

India equity market synopsis

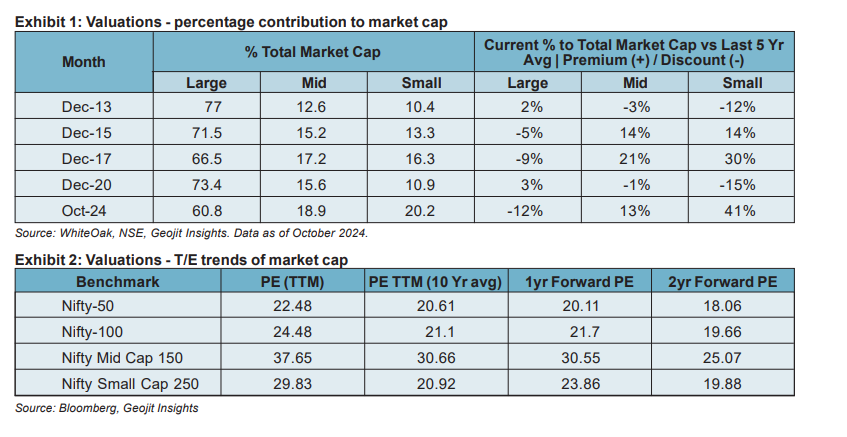

Valuations

Large Cap Market Cap to total Market Cap is the lowest ever at 60.8 percent (discount of 12 percent Vs the last 5-year avg.). Mid and Small caps are trading at a premium of 13 percent and 41 percent respectively Vs their respective 5-year average. India’s current Market cap to GDP ratio (Buffet Indicator) read at 144.5 percent vs its 10-year average of 89.1 percent. While this number has been on the rise, the market cap of mid and small-cap space has outpaced large caps (Historical market cap to GDP for ex-Nifty 50 cos: 35.4 percent vs 79.8 percent currently).

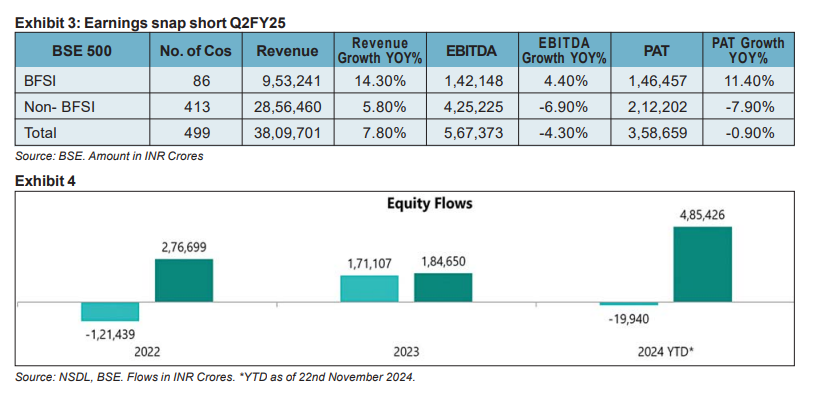

Earnings

The corporate earnings scorecard for 2QFY25 thus far has been weak, impacted by the power and refineries segment. Banks, IT, Pharma, and Capital Goods performed well. FMCG and Automobiles sales have shown weakness. Leveraged companies have shown signs of strain.

Flows

Domestic investors have neutralized the effect of FII equities flows over the last 2 years (Exhibit 4). Alternatively, FII inflows are positive in the fixed income segment for YTD 2024 and are likely to stay robust given India’s bond inclusion in global indices.

Global markets synopsis

With Donald Trump resuming office in January 2025, expectations for ‘America First’ policies may enhance equity market sentiment and strengthen the US Dollar, potentially leading to capital outflows from emerging markets and driving various strategic re-alignments. The US Federal Reserve is expected to cut interest rates by 200 to 250 basis points by December 2025. Meanwhile, China has lowered its benchmark lending rates and introduced stimulus packages to address deflationary pressures. The European Union (EU) may impose tariffs on U.S. goods, impacting industries such as automotive and steel, and potentially slowing European growth.

Five guiding principles for investors on next steps:

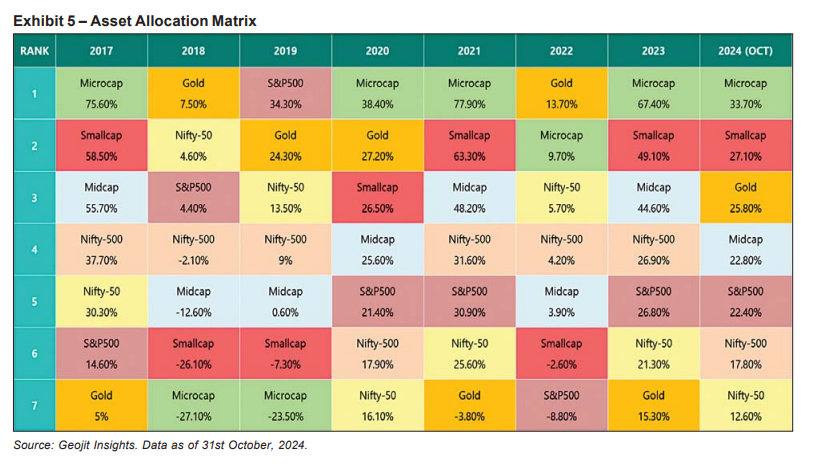

- Portfolio review and asset allocation reassessment: It’s time to review and realign your asset class (Exhibit 5) and market cap allocations to reflect your investment goals, current valuations, and future earnings potential. For instance, the allocation to small and mid-cap stocks may have soared since 2020. Certain sectors have surged over the last 1.5 to 2 years compared to their performance over the past decade. It’s crucial to recalibrate your investments to prevent recency bias; remember, mean reversion is a reality.

- Sizing your bets wisely: Be thoughtful about your investment sizes and avoid a long-tail approach. Tail holdings (under 1 percent of your portfolio) contribute little to overall returns. Don’t hold onto stocks or funds solely because of low prices or NAV; this doesn’t mean they’re undervalued.

- Diversification: Enhance risk-adjusted returns by diversifying across uncorrelated asset classes and creating satellite portfolios that capture tactical opportunities. A well-diversified strategy helps mitigate risk while capitalizing on market changes. For instance, investing across 5-6 mutual fund schemes in the Midcap MF category doesn’t qualify for diversification. One needs to check the overlap across funds to identify the dilution.

- Beware of False Narratives and FOMO: Avoid investing in thematic Funds, IPOs, SME Companies, Microcaps, or Cryptos without proper due diligence. Similarly, a “Buy and Hold Forever” approach may be detrimental to your portfolio if not exited at the right time. Recognize that investment styles (Growth vs. Value), sectors, asset classes, and market caps operate in cycles. A diversified approach provides a better result.

- Return Expectations – The market has seen remarkable returns over the past 3 to 5 years, particularly since the COVID lows, with mid-and small-cap stocks excelling. In the long run, stock prices align with corporate earnings, which for Indian corporations have averaged a robust 12 percent to 15 percent growth. We expect returns to normalize over the next 12 months due to stretched valuations, a slowdown of earnings, and global geopolitical tensions.

Opportunities: Where to invest (new and re-investment post-portfolio review)

Equities

We remain neutral on Indian equities with a preference towards large caps (higher margin of safety) and marginally underweight on Mid and Small caps. The average number of holdings in mid-cap (71) and small-cap (86) mutual funds has increased to mitigate short-term risks. Returns from equities are expected to be more stock-specific in the near-term vs broad-based. We are positive on selected bets across BFSI, IT, Pharma, Consumption, and Infrastructure. We suggest taking a staggered deployment approach over the next 6-8 months to manage volatility. Additionally, US equities and curated emerging market solutions can be a part of the satellite portfolio.

Core Strategies

- From a mutual fund perspective, we prefer Large Cap, Flexicap, Multi-asset, Balanced Advantage, and Multi cap funds.

- Allocation in mid and small cap categories through high-conviction bespoke solutions. It must be staggered over the next 6-8 months.

- Alternative investment solutions like Long/Short strategies have relatively lower net equity exposure than long-only funds. Long-short strategies generate returns by both, going long and short on stocks or index. This approach helps in reducing the directional long-only equity risk and aims to deliver better risk-adjusted returns (lower volatility and higher Sharpe ratio) in the current market environment.

Satellite Strategies

- Developed markets – US markets have been trading above their long-term averages especially in the tech segment. We anticipate strengthening of the US Dollar coupled with pro-American policy announcements would spur US equity markets over the near term (Tactical position for 20-24 months. Prefer staggered investment approach over next 4-5 months).

- Emerging market-oriented funds (ex-India)- While we anticipate a strengthening US Dollar could potentially lead to capital outflows from Emerging markets, there are still pockets that are attractive from a valuation perspective with a favorable risk-reward ratio over the next 36-40 months. Emerging markets would be an opportunistic value play.

Fixed income

While Trump’s policies may pressure the fiscal deficit (medium term), the US Federal Reserve aims for 200-250 basis points in rate cuts by December 2025, focusing on a 2 percent inflation target. A similar easing approach is expected in emerging economies, including India. A diversified dollar bond portfolio focused on investment-grade papers with a duration of 3-3.5 years would be an ideal allocation gaining from locking higher yields and capital gains. Important to note here is that this tactical allocation is not a linear return trade and bond prices can be volatile.

At Geojit, we strive to optimize long-term returns while preserving capital. Our strategy begins with effective asset allocation, followed by tailored solutions to generate alpha and rigor around portfolio review. This scientific approach helps our investors to navigate the various asset classes, especially during volatile times.