It could be argued that the rise in derivatives volumes is not surprising, given the explosive interest in stock market lately, especially after 2020. But, not very long ago, and old timers will surely know that there was a time when stock brokerages had a tough time selling Mutual Funds, especially during downtrends. Today, most know the virtue of persisting with SIPs or Systematic Investment Plans of MFs, especially during downtrend, an affirmation that Mutual Funds sell themselves. Why, some statistics evidence even point to Indian households shifting savings away from bank deposits to Mutual Funds, but a time series analysis done by Bank of Baroda economist failed to find a causality between the two assets, thus failing to establish a clear correlation between the two. One of the attributed reasons why the long-term time series did not show a significant trend for Mutual Funds is the fact that the rise and popularity especially since 2020, makes the Mutual Funds’ trend, a more recent phenomenon when compared with bank deposits.

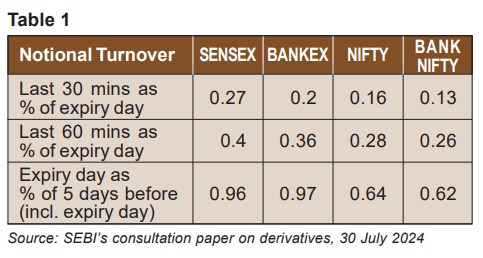

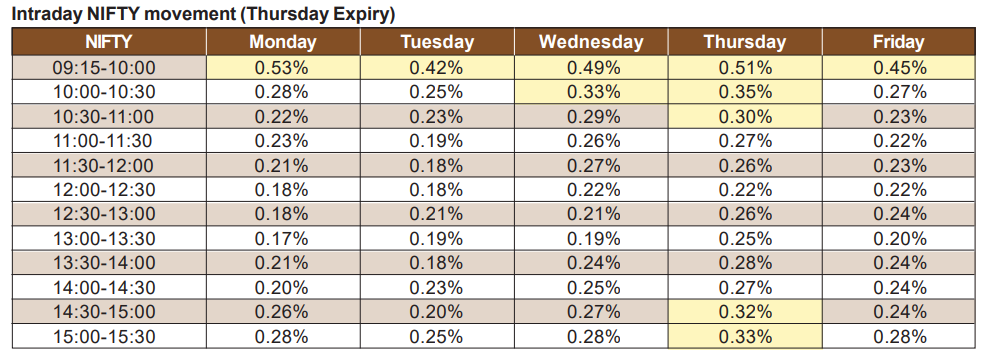

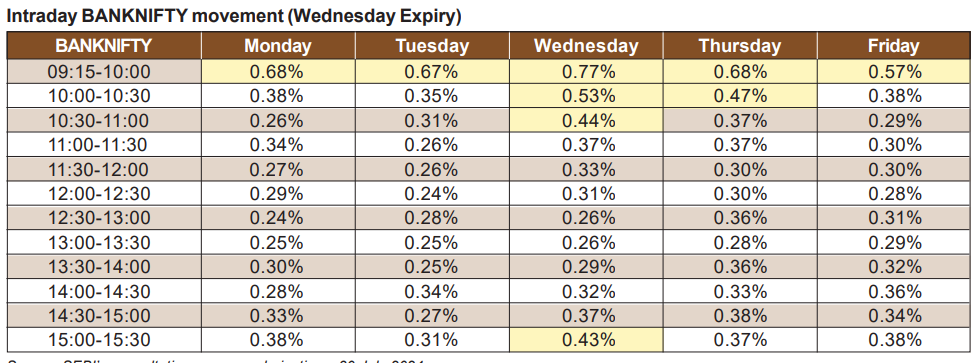

But consider this. The rise in demat accounts since 2020 has been dramatic – From 4.09 crores by end of FY 2019-20 to over 16 crores. But so has been many aspects during this phase, say for example, the rise in UPI transactions which exploded from 1.2 billion in March 2020 to 14.4 billion in July, possibly pointing to change in payment patterns, especially in the P2P (person to person) and P2M (person to merchant) segment. Read these along with the fact that the average age of Indians is under 29, in an age, where almost everything has become shorter. Look at communication via X (formerly twitter) that has a character limit, or even job tenure, which has shrunk to 18 months, according to a moneycontrol article. And large rise in stocks that used to take several years, are happening within a year, some within few months or lesser, effectively shrinking your long term expectations. So, don’t you see it? A lot has changed. So, to link rising popularity of derivative instruments with losses incurred by investors, leaves lot to be desired. But SEBI is absolutely right in looking for a course correction, by acting when the market is strong, rather than being late, especially given the trend in turnover and movement on expiry days. See Table 1 and Table 2.

Table 2

Let us now look at the measures proposed to be implemented in the derivatives segment according to the discussion paper released by SEBI on 30th July 2024.

Measure # 1: Rationalisation of strike price for options

SEBI’s contention is that, having a large number of strikes with very wide coverage could scatter trading activity / liquidity across multiple strikes which could cause sudden price movement in those options contracts. This may also create a possibility of artificial trades in illiquid strikes, at very low option premium. This is plausible, given the fact that weekly contracts have such a short tenure. But more important is SEBI’s finding that, there is a significant quantum of new positions created by participants on the day of expiry in the options strikes which are more than 5% away. On the face of it, the trader’s preference for farther strikes appears to be a matter of price attractiveness, and it remains to be seen, if making it relatively more expensive will suffice.

Measure # 2: Upfront collection of options premium

For futures as well as option shorts, this stipulation is already in place, but any discouragement that will serve as an alert towards undue leverage for option buyers, as they constitute the bulk of new traders, is welcome, though we believe a large section of brokers already insists on upfront margin.

Measure # 3: Removal of calendar spread benefit on expiry day

This strikes at the root of volume multipliers. At present, margin requirement for an F&O position reduces significantly by offsetting position on a future expiry as calendar spread margin applies on such position instead of normal margin on two positions. At the present level of hyperactivity on the expiry day, the risk due to huge price discrepancy between expiry contract and spot or far month contract is high, and the calendar spread benefit that is sensible on other days, may serve only to magnify such risks, supporting this proposal.

Measure # 4: Intraday monitoring of position limits:

This is warranted by the fact that SEBI found of possibility of undetected intraday positions beyond permissible limits as end of day open positions would be NIL, particularly on the day of expiry. Presently, these limits are monitored by MIIs (Clearing Corporations/Stock Exchanges) at the end of the day.

Measure # 5: Minimum contract size

SEBI argues that the minimum contract size requirement for derivative contracts (i.e. `5 lakhs to `10 lakhs) was last set in 2015. During the last 9 years, the benchmark indices have gone up by nearly 3 times. It remains to be seen if it brings in wider bid ask spread that may counter the benefits. SEBI proposes a minimum value of the contract size between 15 to 20 lakhs at introduction time, and which needs to be between 24 to 30 lakhs in 6 months.

Measure # 6: Rationalization of weekly index products

At present, there is expiry of weekly contracts on all five trading days of the week across different indices/exchanges, arguably sustaining speculative activity on all days. Earlier there used to be just one expiry day, which fell on the last Thursday of the month, with indices limited to Nifty and Bank Nifty. Beyond doubt, one of the major tipping point of present move around derivatives is the proliferation of weekly options. So, a reduction of the same will certainly reduce speculation to that extent. But it seems, this will impact the exchanges’ profitability first, as some are very popular and long running products, and then there is the case of Funds or structured products that are linked to some of the popular indices that may have to be retired.

Measure # 7: Increase in margin near contract expiry

SEBI’s contention is that trading activity, quantum of open positions and volatility increase around expiry however the same is not factored in the form of increase in the margin to account for increased risk or to act as a deterrent or to build additional buffers to absorb sudden price shock or volatile black swan event impacting asset markets. Raising margin is a time-tested practice across globe to reign in volatility. The proposal is to raise margins in a measured manner on the day before expiry as well as the expiry. Be sure to see some of the liquidity going away from expiring contracts, but it remains to be seen if they would just land on the nearby contracts itself, and thus recreating a new cycle of entry and exit, with bouts of higher activity still surfacing at a different point than earlier.

Time will tell. SEBI has indeed taken the right step in addressing the questions, but be sure to see more fine tuning, on the go.