Market dynamics and supply challenges drives India’s natural rubber to 12-year high

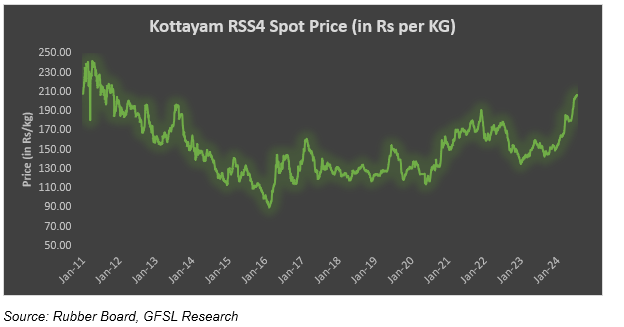

After more than a decade, natural rubber in the Indian market has crossed Rs 200 per kg mark. The benchmark RSS4 grade rubber in the key Kottayam market is hovering near its strongest level in more than 12 years driven by supply-demand imbalances. Natural rubber (NR) prices have started shifting its trajectory on altering supply-demand dynamics, after bottoming out during the 2020 as the Covid-19 pandemic hit globally.

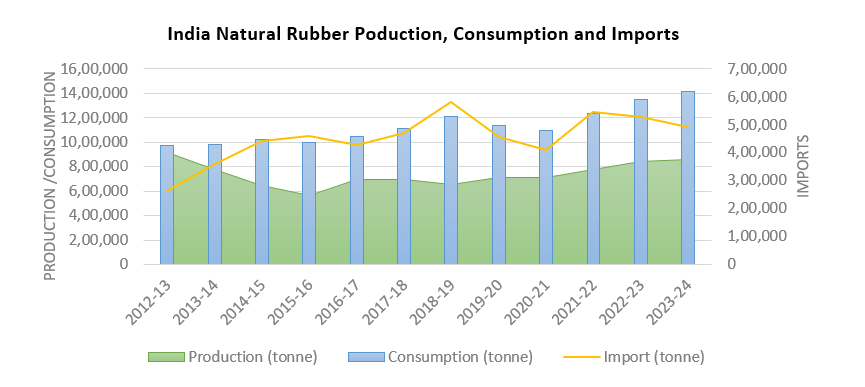

NR output in India continues falling short of demand

Natural rubber is considered as one of the important strategic raw materials with wide range of application in various forms in industries ranging from defence, transportation, healthcare, household etc. While India continues to be the second largest consumer of natural rubber globally, the country’s ranking in terms of production has been descending. A decade ago, India was positioned as the fourth largest producer of natural rubber globally and was pushed lower to the sixth position till 2022 before moving one notch higher in 2023.

Natural rubber output had peaked during the year 2012-13, when the production stood at 9,13,700 tonnes and since then it has been on the lower side, ranging between six to eight lakh tonnes a year. Lower production of natural rubber is being witnessed in the country even though area under natural rubber and tappable areas are on a rise. Rising production costs, unavailability of skilled labour, cheaper imports, changing weather and climatic conditions, weather vagaries in the major natural rubber growing state of Kerala, pest attack and diseases, falling yields, slower pace of planting and replanting etc have caused a contraction in natural rubber output in the country. Prolonged weakness in prices along with rising costs also saw growers abandoning plantations, shifting to other crops, or reducing number of tapping days. However, expansion of rubber planting in non-traditional areas like North-eastern states, measures taken by the Board to increase production and productivity like supply of inputs, especially rain guarding materials through Board promoted companies, continuation of Rubber Production Incentive Scheme, promoting self-tapping so as to reduce the cost involved and thereby increase the profit, adoption of untapped area into tapping etc have helped to raise production to a certain extend.

In the meantime, natural rubber consumption has been mostly on a rise with and exception during the FY 2019-20 and 2020-21, when it showed two consecutive years of decline. According to the Rubber Board of Indian natural rubber demand revived and in the year 2023-24 hit an all-time high of 14,16,000 tonnes, a robust rise of nearly five per cent compared to 13,50,000 tonnes consumed in the previous FY. While demand from the demand from the Auto Tyre and Tube segment stayed steady, a jump of over fifteen per cent was seen in offtake by the General Rubber Goods sector in FY 2023-24 following a twenty per cent in the previous fiscal.

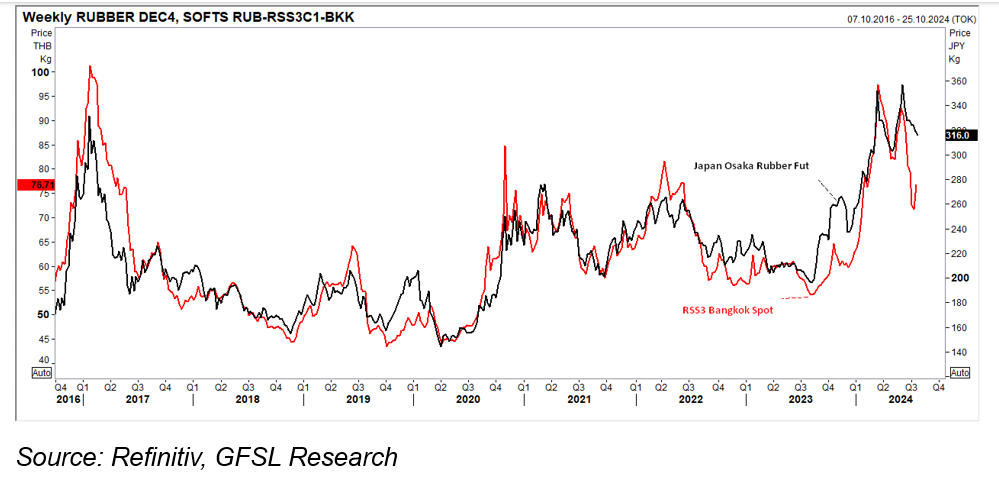

Rise in natural rubber prices in the global market

Global natural rubber prices are on a firmer footing this year as demand is seen surpassing output in 2024 as well. Japan’s Osaka futures hit seven-year highs in March this year and has so far gained about 20 per cent this year. RSS3 grade rubber in the Thailand’s Bangkok spot market breached 100 baht per kg for the first time since February 2017 in March this year before trimming gains.

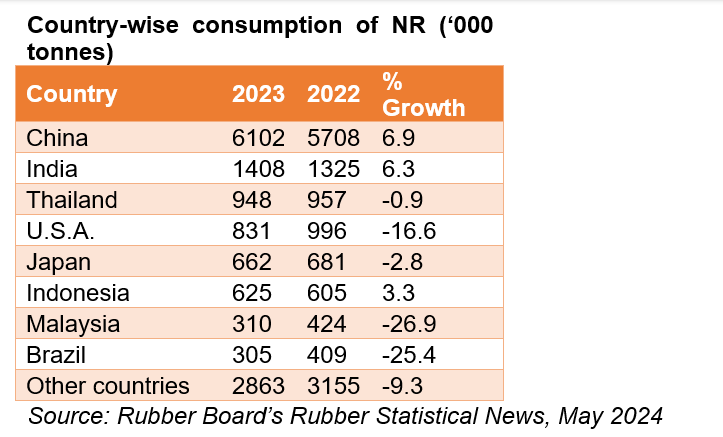

According to the International Rubber Study Group (IRSG), strong recoveries and consumption demand in emerging markets, particularly China and India, bolstered global rubber demand. Global natural rubber demand grew by 1.4% in 2023, reaching 14.82 million tonnes, primarily driven by the recovering economic activities, and booming electric vehicles market, and sees NR demand increasing by 2.5% in 2024, driven by both tyre and non-tyre sectors.

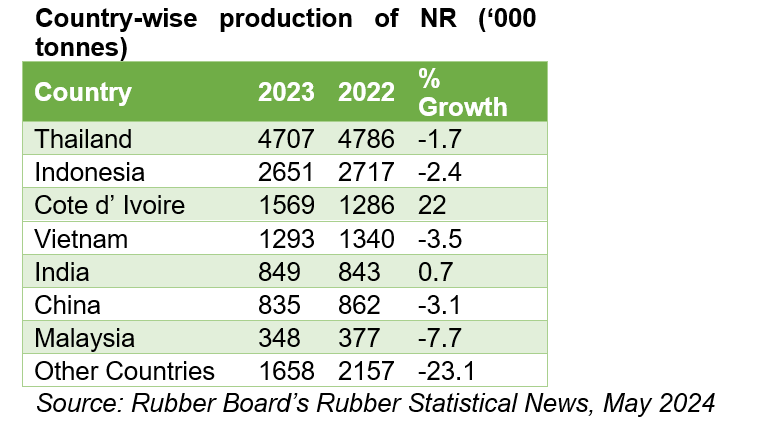

In 2023, global NR production had dropped by 2.0% to 14.08 million tonnes according to IRSG. The decline was mainly due to fall in production in the key NR producing countries like Indonesia, Thailand, Vietnam etc. Extreme weather conditions, especially during the peak production phase (Sep-Oct to Jan) in countries like Thailand, Malaysia, China, Vietnam etc. disrupted tapping and production activities. Spread of leaf fall disease in Indonesia and Sri Lanka also affected yields. Also, prolonged lull in NR prices and higher production cost resulted in low maintenance of plantations or shifting to other remunerative crops. However, the production loss was compensated to a certain extend by jump in output from Côte d’Ivoire (Ivory Cost). In the meantime, NR production growth is estimated to recover to 3.0% in 2024. NR output is expected to continuously expand in countries like Côte d’Ivoire. However, ISRG points out that production gains may not be sufficient to offset the substantial reduction in production forecasted for Indonesia and other Southeast Asian producers, leading to potentially insufficient rubber supply in the medium to long term.

Supply chain disruptions and rising freight cost

Geopolitical tensions in the Middle East, affecting the global trade, have also contributed to the recent surge in natural rubber prices. Red Sea shipping crisis which began last year following the Houthi attacks on ships transiting through the Red Sea have created significant impact on trade between the Asian countries and the West. According to the World Bank report, The Red Sea, a critical conduit for 30% of the world’s container traffic, which is currently facing a shipping crisis of unprecedented scale and is causing a significant downturn in maritime activity. As of end-March 2024, the volume of traffic through the strategic Suez Canal and Bab El-Mandeb Strait has dropped by half, while the alternative route via the Cape of Good Hope route has witnessed a 100% increase in navigation. The longer routes required by the current situation has led to soaring freight rates and shipping insurance costs, contributing to inflation, and negatively affecting regional and international shipping economies. With India depended on imports to meet the surging demand, shipping delays, container shortages and increased demand from the US, Europe, China to stock-up is impacting the landed cost as well.