The significance of large-cap stocks is invaluable. They enhance both the strength and depth of a portfolio. Their superior quality is fortified, especially during volatile and downward market cycles. They significantly contribute to long-term stability. Hence, we foresee the importance of large caps increasing in the coming quarters.

The significance of large caps increases in the context of the risk of global economic slowdown and tight monetary policy, followed by increased domestic volatility and anticipated slower earnings growth in FY25 and FY26. The Indian stock market has seen a steady rally over the past four years, pushing midcap valuations to new all-time highs. The sustainability of this trend will depend on the continuation of bumper earnings growth and domestic inflows, from which it has benefited in the last three years. Large caps are trading securely around their long-term average, with an average earnings growth forecast of 13%, and are well-equipped to manage the global slowdown and the impact of rising commodity prices on profitability. We believe it is advisable to increase exposure to large caps and reduce high exposure to mid and small caps, creating a conservative or balanced portfolio based on your risk tolerance.

The short-term volatility

Since the start of FY25, the Indian market has been dilly-dallying with a lack of clear direction. In the last one-month, the Nifty50 has been trading within a broad range of 1,000 points, between 21,800 and 22,800, awaiting the results of the national election. However, there is no loss to the investors, led by the moderately positive return of mid and small caps edging the broad market. The country’s total market capitalisation has increased by 6%, from Rs. 387 trillion on 31st March to Rs. 412 trillion on 18th May 2024.

In the past two months, FIIs have been selling ahead of the upcoming election results due to the premium valuation of India, while retail investors remain cautious with a bias towards investing in mid and small-cap stocks. Meanwhile, DIIs are accumulating shares, resulting in minor buoyancy in the broader market. However, investors are inclined to sell during rallies as the market remains range-bound and struggles to reach new highs. Additionally, the recent lower voter turnout has added uncertainty to the election outcome. There is doubt as to whether it is due to the heatwave or fatigue in Modi aura. The initial expectation that the NDA would win with a huge majority has moderated due to losing the backing of core BJP supporters. Also, a noticed disorder in political structure in states like Maharashtra, Bihar, Haryana, and Karnataka has added confusion about a positive outcome for the NDA.

Q4 results are better than forecast but haven’t prompted earnings outlook

The significance of Q4 was pivotal in shaping the outlook for FY25. The Q4 earnings have exceeded expectations; PAT was forecast to grow by 12% YoY, but actual growth is 22%, 1,000bps better. Despite the bumper outcome, the market continues to anticipate moderation in FY25 earnings growth compared to FY24. However, there is potential for an upside to this conservative forecast of 13% EPS growth, like what occurred in FY23, due to the constant upgrade in GDP growth.

In April, key domestic economic indicators such as GDP, manufacturing and service PMI, auto sales, and industrial output remained positive. Moreover, domestic CPI inflation showed signs of easing, which is viewed positively for future RBI policy adjustments, potentially paving the way for a rate cut. Loan growth of scheduled commercial banks remains in double digits. Economic indicators continue to be robust, indicating that the Indian market should sustain its buoyancy. However, the market is cautious about earnings growth in anticipation of a slowdown in the global economy and a rise in commodity prices impacting the EBITDA margin.

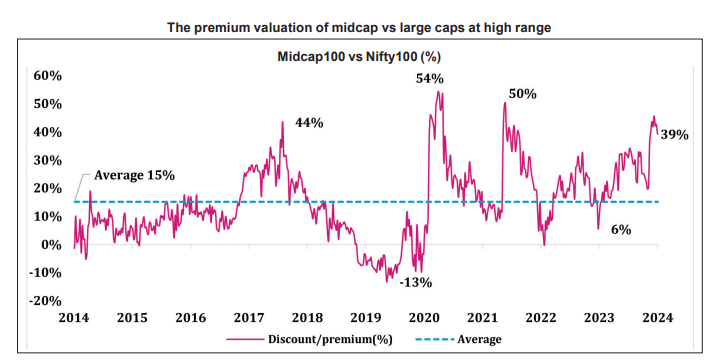

Premium valuation of midcaps

The Nifty Midcap Index is trading at a one year forward P/E of 29x, which is 38% premium to long-term average. The Nifty50 Index is trading at P/E of 20x, around 10% premium to the long-term average, which is sustainable with an upside bias due to a stable earnings outlook. Large caps are viewed as safer, particularly during volatile periods. Hence, it is recommended to reallocate exposure from midcaps to large caps as part of a cyclical restructuring strategy.

The premium valuation of midcap vs large caps at high range

Going forward we have a moderately positive expectation with focus on large caps

Looking ahead, we anticipate a reduction in volatility over the next 1-2 months, with the hindsight of a continuation of the growth policy. However, the initial 2-3 months of FY25 may yield a mixed perspective. The primary driver of volatility is the heightened expectations surrounding the national election outcome, which is prompting selling by FIIs.

The Q4 has concluded better than estimated, providing an insight into FY25 earnings growth. Presently, the market estimates a slowdown in earnings, Nifty50 EPS growth is forecast to reduce from 23-24% in FY24 to 13% in FY25. Consequently, there has been a decline in valuation since the beginning of the year. The Nifty50’s one-year forward P/E has decreased from 23.5x to 20x. India’s historically high premium valuation has moderated to 11% based on the 10-year average P/E of 18x, which is relatively low. We believe that the Indian market is likely to remain in premium valuation due to the outperformance of the domestic economy compared to other emerging markets. With stable long-term earnings growth and fair valuations, we are positioned on a solid foundation.

We believe the Indian economy is forecast to grow at a stable GDP growth rate of an average 6-7% this decade, with an upside risk. However, any further global economic slowdown could trigger short-term valuation contractions. Despite this, the Indian economy is robust, and the RBI has consistently revised its growth outlook upward over the past two years. For FY25 too, there is a strong likelihood of a further upgrade in the forecast of India’s economic growth. It hints at the rising number of new investment project announcements and the completion of new projects in FY24, as per CMIE data. Optimism is expected to persist, driven by the China Plus One strategy and the rejuvenated Make in India policy. The domestic economy is also expected to improve with a boost in growth for the rural economy. The dried-up rural market of 2023-24, due to El Nino, is up for a swing in 2024-25, especially in the agriculture sector. The scenario is estimated to improve in anticipation of La Nina, as per IMD and global climate expectations. The current GDP forecast of 7% growth in FY25 by the RBI may rise to 8%, led by high private capex, foreign investment, and upside in the rural economy.

We like these large caps

Large-cap stocks are expected to offer a buffer against heightened volatility. Encouraging developments are evident in sectors such as manufacturing, capital goods, infrastructure, and energy, all of which are linked to GDP growth. Investors are strategically accumulating positions in sectors such as FMCG and Chemicals, which are currently undervalued relative to their long-term metrics, and stand to benefit from potential catalysts such as improvements in global and rural demand.

Sector-wise, positive momentum is evident in FMCG and auto stocks, driven by expectations of a revival in rural demand in H1FY25. The FMCG sector is anticipated to see improved performance as the IMD has predicted a normal monsoon, which should drive strong agriculture and reduce input prices. Conversely, PSU banks are underperforming in the short term due to the RBI’s tighter lending norms for projects under development. IT and Pharma have a good long-term investment horizon with a medium-term focus on mid-tier companies, as they are sustaining growth better than large caps, and valuations are deemed fair. The financial sector is also likely to benefit from India’s long-term growth story. Currently, we prefer large private banks and NBFCs compared to PSU Banks, and mid and small tier financial companies.